Negative gearing arouses passions on both sides: about a third think people are making legitimate deductions, a third think it’s a rort, and a third don’t know. This blog explains how negative gearing works, to help resolve these issues. A more complete analysis of negative gearing can be found in a recent ACOSS report, “Fuel on the fire”.

Category Archives: employment

Hidden gems in the Tax Discussion Paper (2): we don’t rely a lot more on income tax than other countries.

Reading the press you’d think a key message from the Govt’s Tax Discussion Paper is that Australia relies a lot more on income tax than other wealthy countries. Not so! Read the fine print and we find that 63% of public revenue in Oz comes from income and income-like taxes compared with 61% across the OECD.

Racing against time: indexation of social security payments

Indexation of social security payments is a dry subject. Does it really matter if they’re indexed to MTAWE or CPI? You bet! The Government’s budget proposals to index pensions only to the CPI and not to wages would reduce them by $80pw in a decade compared with present indexation, and save a motza. The Rudd Government’s decision in 2009 to index family payments to CPI instead if wages has saved over $1B and has already cost a low income family with 2 children under 13 years $19pw. If Newstart Allowance had been indexed to wages as well as the CPI over the last 20 years, it would now be $115pw higher ($52 instead of $36 a day).

Hidden gems in the Tax Discussion Paper: Shocking news from Treasury – personal income tax as efficient as GST!

Business, Government, and “every pet shop galah” have been saying that we should rely less on personal income taxes and more on the GST because this would be good for the economy. In my blog ‘Who’s the fairest and most efficient of them all?” earlier this year, I challenged this view.

Treasury modelling of the economic impact of different taxes tucked away on p32 of the Government’s Tax Discussion Paper confirms my doubts. It should change the debate.

Now, Treasury has released the details of that modelling.

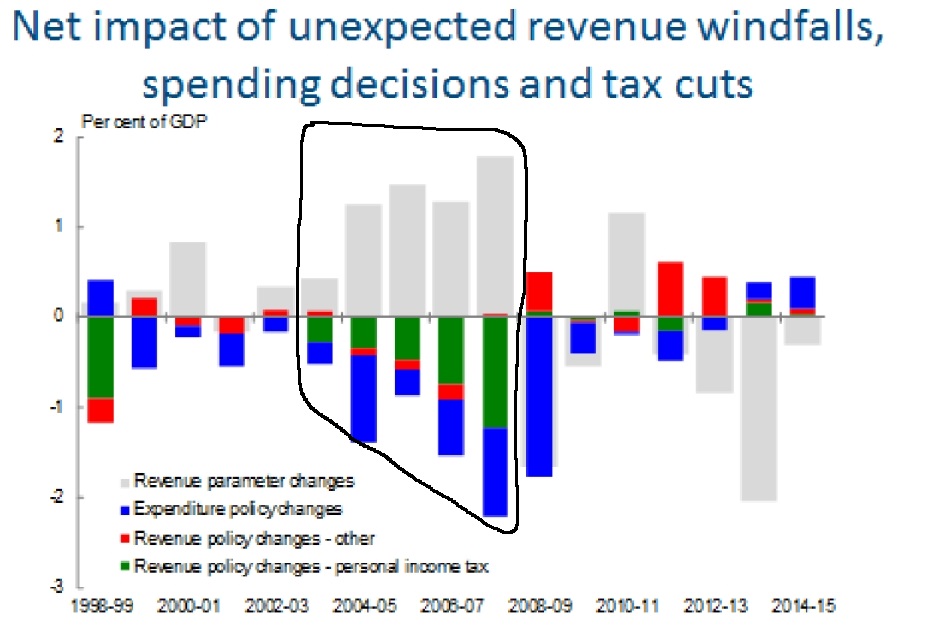

How the Budget was mugged (Treasury publishes the photo)

New Treasury Secretary John Fraser’s first speech includes a picture showing how the Federal Budget was mugged during the mining boom:

“The start of the structural deterioration in the Commonwealth’s budget position began

before the global financial crisis.”

The following chart, included in his slides, shows how the windfall revenue gains from the boom between 2002 to 2008 (grey bars, circled by me) were spent (green, blue and red bars).

Bulging with company tax and capital gains tax revenues, the Federal Budget was mugged on its way to the bank and the proceeds spent equally on eight successive tax cuts (green bars) and spending programs (blue bars) that were often of dubious value – including the Seniors Supplement and easing of pension asset tests for wealthy older people in 2007, and the Education Tax Refund in 2009.

“The green and blue bars below the line show that these positive revenue surprises were largely handed back through personal income tax cuts or spent.”

By 2009 it was all over. The then Government tried valiantly (and succeeded) to avoid a recession through stimulus spending which was later wound back (the blue bar outside the circle).

Fraser didn’t put much emphasis on the fiscal damage caused by those tax cuts (he’s from Treasury), except to point to another well known story – the waste of revenues in poorly targeted tax breaks for superannuation:

“Generous income testing arrangements for Family Tax Benefits in the early 2000s and access to million dollar contributions to tax-preferred superannuation through 2006-07 were notable examples of middle or higher income welfare that contributed to the problem.”

As the ACOSS submission to the Audit Commission argued, these Budget decisions had huge opportunity costs. Instead of well targeted spending to deal with pressing problems – poverty, unaffordable housing, and the gaps in community services for people with disabilities and mental illness; people who had no need of more public support were offered ‘bonus’ payments and fresh opportunities to avoid income tax in old age.

Future generations will pay for all this if the most wasteful and profligate Budget decisions aren’t reversed. We’ll also pay a high economic and social cost if the harshest savings measures in last year’s Budget aren’t abandoned, starting with the denial of income support for unemployed young people. That Budget did include sensible measures, such as the removal of the Seniors Supplement, which should go ahead.

The bottom line though, is that Australian Government spending is for the most part well targeted (the graph below shows that our cash social security spending is third lowest in the OECD) a major reason Oz Governments spend less than most other wealthy countries. A Budget repair job which is confined to the spending side (as in 2014) will either fail (as in 2014) or cause social harm.

If we are to provide the health and community services needed by an ageing population, Australian (and State) Governments will have to raise more revenue, and learn to do this in a more economically efficient way. [No, I’m not ‘jumping to the GST conclusion’. Let’s open our minds a bit. Take a look, for example, at the reforms being discussed in South Australia].

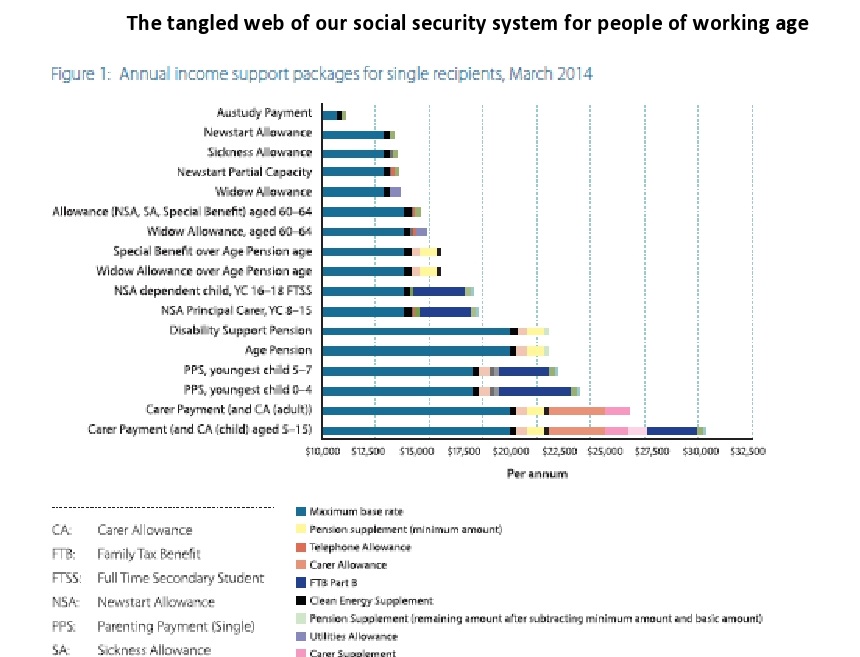

Not as simple as it sounds: The Welfare Review in pictures

The Welfare Review Report has finally been released. It advocates a “new flexible social support system that is simpler, sustainable, coherent and outcomes focused”.

The Review proposes to replace the present tangled mess of 20 income support payments paid at various levels (see figure)

with ‘five main payments’ (see figure):

- Tiered Working Age Payment

- Supported Living Pension

- Child and Youth Payment

- Carer Payment

- Age Pension.

Sounds good, and a welcome change of tone from last year’s Budget. But unscrambling this egg is not as simple as it sounds, and nor is the recommended payment structure.

Long term unemployment: ‘achilles heel’ of the Job Services Australia model

The following is a paper I presented at the long-term unemployment conference in 2014. It argues that the fact that two thirds of people on Newstart Allowances have received it for over a year and half for over two years signals policy failure. Governments have failed to invest in the regular work experience, training and capacity-building, and connections with employers needed by most people who have been out of paid work a long time.

JSA (and before that Job Network) rewards providers for low-level job search assistance. Average caseloads are over 100. This might work when people are close to employment already, but it’s not good enough for those with low skills, weak (or no) employment experience, or a disability. In theory, paying providers according to job outcomes is a good idea, but as in other countries where this has been tried, it hasn’t worked out as the policy makers planned. To begin with, Governments only get the quality of employment services they are prepared to pay for. In Australia they have not been prepared to pay for it.

The previous Government built a program based on short-term low quality training (average spend $300 per course, % employed after course 30%). The present Government is building a new one based on Work for the Dole (average spend $2,000, % employed after program 23%). Neither approach was successful (except in the sense that it kept unemployed people busy).

Is there a magic pudding? A quick analysis of CPA Australia’s GST proposals

This is a quick off the cuff analysis of CPA Australia’s report: Tax reform in Australia, the facts, a day after its release. In the absence of time to study the report more closely, and critical details of the modelling and presentation of data, I raise as many questions as answers. But they are important questions – including how a revenue neutral change in the tax system leaves all households better off. There are efficiency gains from good tax reform but the magic pudding remains elusive!

The CPA proposals are a welcome change from standard ‘tax mix shift’ reform proposals which trade off a higher GST for lower income taxes. Instead, most of the revenue gained from higher GST would be used to remove some of the most inefficient (and unfair) State taxes such as Stamp Duties on insurance. Aside from the proposed income tax cuts, most of the taxes to be replaced fall mainly on household consumption, so the implications for the distribution of spending power among households are less clear cut than a straight consumption tax for income tax switch, which is strongly regressive. See my previous blog ‘Who’s the fairest of them all’ and ACOSS analysis ‘Paying our fair share’.

The CPA advances four reform options:

- A 10% GST with health, education and fresh food exemptions removed to raise $12B in 2015 to replace stamp duties on insurance & motor vehicles ($8B) and modestly reduce property Stamp duties and other indirect taxes ($2B), with the remaining $2B used for income tax cuts and an increase in income support payments.

- A 15% GST off the existing base to raise $26B to replace stamp duties on insurance & motor vehicles ($8B), substantially reduce property Stamp Duties ($10B) and other indirect taxes ($2B), with the remaining $6B used for income tax cuts and an increase in income support

- A 15% GST with health and education in the base to raise $37B to replace stamp duties on insurance & motor vehicles ($8B), abolish property Stamp Duties ($13B) and other indirect taxes ($2B), with the remaining $14B used for income tax cuts and an increase in income support

- 15% GST with health education and fresh food in the existing base to raise $42B to replace stamp duties on insurance & motor vehicles ($8B), abolish property Stamp Duties ($13B) and other indirect taxes ($2B), with the remaining $19B used for income tax cuts and an increase in income support.

Using a model developed by KPMG, the report estimates the impact of these options on economic growth and on households (divided into groups of 20% by household ‘equivalent’ income). It also makes a number of claims about the inefficiency of the current tax ‘mix’. This blog is in two parts: ‘what’s clear’ (some obvious points) and ‘what’s not clear’ (questions that need to be clarified).

What’s clear

1. Australia does not rely a lot more on income taxes (broadly defined) and a lot less on consumption taxes, than the OECD average.

The international tax revenue data in the report shows that, when social insurance contributions in other OECD countries are added in, 58% of tax revenue in Australia comes from taxes on income compared with an OECD average of 60% – or 63% compared with 61% if Payroll taxes are included (figure 2-8)

The share of tax revenue raised from consumption taxes is 27% in Australia compared with an OECD average of 33%. There’s much more to consumption taxes than GSTs and VATs, including State taxes such as Stamp Duties that fall on consumption.

2. The increases in the GST modelled for the report by KPMG would reduce economic growth for the first three years after the reform.

It is well known that one of the short term effects of an overall rise in consumption taxes is that the economy slows, due to the impact of higher prices (just ask the Japanese). To be precise, it increases household consumption in the years between announcement of the reform and implementation as people rush to buy good at existing prices, then reduces it).

3. Abolishing inefficient State taxes would boost growth in the long run

It’s not surprising the modelling finds that GDP would grow faster over the long term if these taxes were abolished. Taxes such as Stamp Duties have well known negative impacts on investment and growth. Taxing business ‘inputs’ rather than final income or consumption or assets such as land and mineral wealth is inefficient as it distorts household and business investment decisions (for example by discouraging people who need it from taking out insurance, and penalising decisions to move house).

The $27.5 billion dollar question is: by how much? This is notoriously difficult to estimate. As with all macro-economic modelling, results depend on assumptions. The report appears to take this a step further by assigning the projected economic efficiency gains to households (which no Government would be brave or foolish enough to do).

4. Low income households don’t usually benefit from tax cuts

One quarter of households, including the vast majority of those in the bottom 20%, pay no income tax (but they do pay consumption taxes), so they would be worse of in the absence of social security payment increases if consumption taxes increased.

As the above ACOSS report argues, relying on social security payment increases to sustain spending power is risky in an environment when these payments are under threat (see last year’s Budget)

What’s not clear

1. Why do all households gain from revenue-neutral tax reforms?

All four proposals are revenue neutral. They neither increase nor reduce taxes overall. So in the short term, reform is a zero sum game with winners and losers. Yet all households appear to win in the modelling.

A close look at Appendix ‘C’ shows that his happens because of a line item called ‘increase in income before tax’. Why would income increase before tax (apart from social security payments increases which are accounted for separately)?

One possible reason is the claimed ‘efficiency dividend’ from the reform. That is, the economy grows more quickly because taxes are less distortionary. But that’s a long term impact. As indicated, the model shows that GDP growth slows for the first three years and household consumption is projected to fall for the first five years.

If ‘input taxes’ (such as Stamp Duties) are replaced by a tax on consumption (like the GST) we would expect households to be slightly worse off in the short term, in the absence of compensation. This is because in the short term, some of the gains from abolition of input taxes would ‘leak’ to sectors other than Australian households (especially exports).

2. What happens of we exclude ‘increases in income before tax’ and focus on the impact of the tax changes?

If we separate out the effects of tax and social security changes (higher GST, lower Stamp Duties, and income tax cuts and social security increases) from the projected ‘increases in income before tax’ we find that the first reform option (removal of GST exemptions, abolition of some Stamp Duties, a reduction in the first marginal tax rate from 19% to 18.5%, and modest social security increases) reduces household spending power for the bottom 2 quintiles and raises it for others.

This is the pattern of short-term winners and losers we would expect from such a change (red bars), though the average losses at the bottom end are much larger than expected:

- Low income households are disproportionately affected by the consumption tax changes

- Since only the lowest marginal income tax rate is cut, middle income households gain the most, but high income earners also gain because the tax cuts flow through to them as well.

When the ‘increases in income before tax’ are added in (blue bars) everyone wins and the reform is distributionally neutral (see Figure 3-4 in the report).

But where do these income increases come from? The report refers to ‘increased incomes as a result of improved efficiency in the economy’ (p14). If this is where they come from (and these look like brave assumptions), how would these efficiency gains flow through to households in the first year of the reform (2015-16)?

3. What is the effect of the consumption tax changes on their own?

It would be worth knowing what the effect of replacing Stamp Duties with a higher GST has on the spending power of households at different income levels, since this kind of reform is rarely modelled. The impacts are not obvious since Stamp Duties themselves largely fall on household consumption – so the reform would replace one set of regressive taxes with another. Its effects would depend on the spending patterns of different households (e.g. on food, home purchases, car purchases, insurance, etc).

It’s good to see more information out there on the impact of different tax reforms, and it would be even better if some of the results in the report were explained more fully.

ACOSS report shows taxes are lower and less progressive than people think.

A new ACOSS report released this week looks at how overall rates of tax vary among households, according to income. It follows on the heels of a claim by the Treasurer, Joe Hockey, that middle income earners pay half their income in taxes. Borrowing from ‘tax freedom day’ campaigners, he claimed we work six months of every year for the Government (though they reckon it’s all been paid off by April).

This surprised pretty much everyone who knows the difference between marginal tax rates and average (overall) tax rates (the marginal tax rate is only paid on that part of your income above your highest tax threshold, not all of your income).

Using published ABS data, the ACOSS report shows that middle income households paid a total of 23% of their gross incomes in tax in 2010, comprising 11% income taxes and 12% taxes on consumption. About half of Hockey’s 50%.

But the real story of the ACOSS report is how the progressive effects of the income tax are almost offset by the regressive taxes on consumption.