Reading the press you’d think a key message from the Govt’s Tax Discussion Paper is that Australia relies a lot more on income tax than other wealthy countries. Not so! Read the fine print and we find that 63% of public revenue in Oz comes from income and income-like taxes compared with 61% across the OECD.

What the Govt’s Tax Discussion Paper says about our reliance on income tax

When he released the Tax Discussion Paper at an ACOSS function last week (the one oddly titled “Rethink” – Rethink what? Most of the work was done in the Henry Report), Treasurer Joe Hockey repeated the hoary old argument that Australia relies too much on income taxes:

“Australia’s heavy reliance on income taxes may be unsustainable”

I pointed out in my last blog that the Discussion Paper found that personal income tax is no less efficient than the GST, though company income taxes detract more from economic growth.

But there’s another factual problem here: we don’t rely a lot more than other OECD countries on income taxes, when apples and compared with apples.

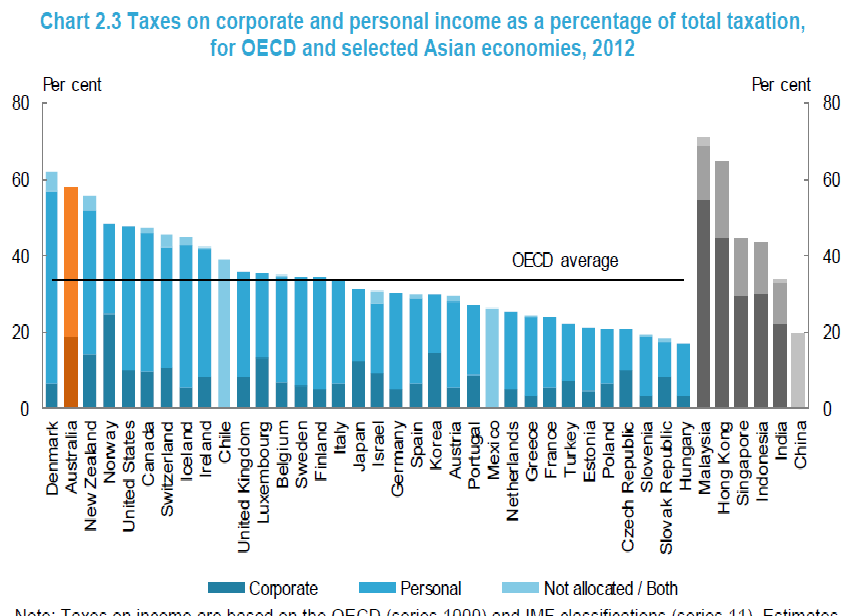

The claim that we rely heavily on personal and company income taxes is illustrated by this graph in the Report. It compares revenue from personal income and company taxes for all levels of Govt across the OECD. On this count, we’re second highest to Denmark (see yellow bar).

The Discussion Paper notes that:

“Australia relies more heavily on income taxes on company and individual income (often

termed ‘personal income tax’, including by the OECD) than other developed countries (Chart 2.3)

There’s a problem with this comparison. One of the things we have in common with Denmark is that we don’t levy social insurance taxes to pay for public pensions and unemployment benefits. Most OECD countries do. These are taxes on income, and should be included.

In its next graph, the Discussion Paper includes social insurance taxes, and also Payroll Taxes which have a similar purpose (Payroll Taxes are ultimately a tax on wages. They were introduced in Australia to finance Child Endowment). Here the story changes. We’re close to the middle (yellow bar); with 63% of public revenue coming from these taxes compared with 61% across the OECD.

The Discussion Paper notes that:

“Direct forms of taxation — individuals and corporate income taxes, compulsory social

security contributions plus payroll taxes — comprise around 63 per cent of taxation in

Australia. This compares to the OECD average for direct taxes of 61 per cent (Chart 2.4).”

Some argue that our Superannuation Guarantee should also be included, and that this would raise our reliance on income taxes overall. The trouble with that argument, as the Discussion Paper points out, is that:

“Australia’s compulsory superannuation system — the superannuation guarantee — is

sometimes equated to a social security tax. However, as it is paid directly into private

superannuation accounts (currently set at 9.5 per cent of an employee’s ordinary time

earnings) rather than to the government, it does not meet the definition of a tax.”

Put this together with the fact that Australia has low tax revenue overall (seventh lowest in the OECD, see the yellow bar), and our overall reliance on income taxes doesn’t look so high.

Our reliance on company income tax is above average (second to Norway). What do have in common with Norway? A profitable mining industry. Our company income tax is in part, a tax on mining rents (recall that the Henry Report proposed to replace part of it with a Resource Rent Tax).

Company tax revenue boomed from the early 2000s, just as the mining boom hit its straps (see the yellow line). Large reductions in iron ore and coal prices in recent years have hit company income tax revenues hard, and this is the main single cause of our present Budget problems.

Those Budgetary problems are getting worse. While we clearly can’t sit back and wait for income tax bracket creep to sole them, strengthening the income tax system has to be part of the solution.