‘The tax code, once you get to know it, embodies all of the essence of life: greed, politics, power, goodness, charity. Everything’s in there.’ Sheldon Cohen, Former Commissioner of the US Internal Revenue Service.

Tax reform is back on the agenda. Since those who fail to study history risk repeating it (and I was involved in the latter-day history of tax reform) I’m writing this 3 part series as a guide for those involved in the next phase. Parts 1 and 2 dealt with the dominance of income tax since WW2 and the challenge from consumption taxes since the 1970s. This part: the ‘Trojan Horse’ discusses new thinking about taxes and their impact on the economy. It argues that our income tax already incorporates elements of a tax on consumption, that we should move beyond a simple dichotomy (and old arguments) between taxing income or consumption, and explore fresh ideas for reform.

Readers with an interest in the details can check out the references in Parts 1 and 2 of this series. Brooks provides a more detailed presentation of the issues raised in these three blogs. In addition, good summaries of some of the latest ideas in tax reform are provided by Auerbach, Evans, the Henry Report, and Henry. Those wanting to keep up with current Australian tax debates should visit the Tax Watch site.

A recap on the tax wars: income Vs consumption

To recap parts 1 and 2 of this series, the income tax became the main tax in Australia and most wealthy countries after WW2. After the 1970s, as policy makers worried less about income inequality and tax fairness and more about the state of the economy, there was a push to replace income taxes with taxes on consumption. The basic difference between income and consumption taxes is the treatment of investment income. Broadly speaking, this is taxed under an income tax but not under a consumption tax. Income tax advocates argued that investment income should be taxed because this, along with wages, was the best measure of ‘ability to pay’. Consumption (or expenditure) tax advocates argued that consumption was the better measure of people’s resources and that taxing investment returns discouraged saving and investment.

The income tax system continued to dominate the tax landscape, while for 30 years the battle of ideas raged outside. Its ideological champion was the comprehensive income tax: the idea that income from all sources – wages and investments – should be taxed at uniform (progressive) rates. It’s war cry was ‘a buck is a buck’. Advocates argued that the comprehensive income tax was not only fair – because spending power from different sources would be taxed equally. Uniform income taxation was also economically efficient because decisions to work, save and invest would be less influenced by taxes (e.g. people would pay the same taxes whether they invested in property, shares or an active business).

The champions of expenditure taxation took up the fight – in Australia it was the GST, in the US and UK cash-flow or personal expenditure taxes (different warriors, same suit of armour). Their war cry was ‘save and invest!‘ In the 1970s, the Meade Report in the UK and the Treasury in the US argued that by taxing investment returns, income taxes discouraged saving and diminished investment, holding back economic growth. They also challenged the fairness of income taxes, arguing that they were biased in favour of current spending and against saving to shift spending into the future. Their answer was to tax consumption or expenditure instead of income.

A fatal blow to the comprehensive income tax

The fatal blow to the idea of a comprehensive income tax came when the economic efficiency benefits of taxing income uniformly were seriously challenged by ‘optimal taxation’ research in the 1980s and 90s.

Actually, the idea that different activities should be taxed uniformly was challenged as early as 1927 when Ramsey argued that because taxes on different goods have different impacts on people’s spending habits, ‘optimal’ tax rates would vary from one good to the next. If people were less likely to stop buying food in response to a consumption tax than (say) go to the movies, then food should be taxed at a higher rate than the movies. The more responsive an economic decision was to taxation, the lower the tax rate should be, and vice versa. Ramsey was talking here about consumption taxes, but the idea was applied to income taxes as well.

Ramsey’s ‘optimal tax’ theories had little impact on public policy for many years. This was due to concerns about the equity impacts of higher taxes on essentials, uncertainty about the impact of taxes on different activities, and the complexity of a system that would impose different tax rates on different goods, services and incomes. There was also a risk that if tax rates on different activities were ‘up for grabs’, interest groups would lobby all the more vigorously for their own activity to be taxed less (i.e. it would encourage rent-seeking). Nevertheless, a branch of economics called ‘optimal taxation’, inspired by Ramsey’s ideas, grew in influence from the 1970s. It spawned fresh research on the impact of taxes on economic activity.

These studies generally found that taxing all income (wages and investment) uniformly (at flat or progressive rates) was not as efficient as comprehensive income tax advocates made out. They concluded that investment income should be taxed at lower rates than wages. This meant that a comprehensive income tax that was levied at uniform rates could only be defended on equity grounds. At a time when Governments worried more about declining economic growth than growing income inequality, this was a fatal blow to the ideal of a comprehensive income tax, despite the fact that reforms during the 1980s in the US and Australia moved us closer to it.

The problem was not that income taxes diminished saving. The evidence from optimal taxation research suggested that lower taxes on saving impacted people’s choice of savings vehicles (e.g. bank accounts Vs superannuation), but not the overall level of household saving. Further, in an open economy investment could be partly financed from foreign savings.

The problem was that income taxes were likely to discourage investment, especially across national borders. By the end of the last century, the consensus among economists was that more ‘mobile’ economic factors were more sensitive to taxation, and could pass the cost onto less ‘mobile’ factors. Being relatively mobile, capital was more likely than labour to shift to investments (or nations) with the lowest tax rates. Under these conditions, the cost of the company income tax was more likely to be passed on to workers. At the other end of the spectrum, land and mineral resources were said to be immobile. Taxes on these factors were more likely to ‘stick’, and less likely to affect investment decisions.

By the 1990s, the debate among most economists and tax experts was no longer whether all income should be taxed uniformly. It was about whether investment income should be taxed at all, or at a lower rate than wages.

The fatal weakness of expenditure taxes

Despite the defeat of the comprehensive income tax in the battle of ideas, as Part 2 showed the income tax system remained the dominant source of public revenue.

The idea that income taxes should be replaced by a tax on expenditure (viewed as the polar opposite of the comprehensive income tax) had its own fatal weakness. The public still equated ‘ability to pay’ with annual income, and it was clear that those with the lowest annual incomes would be adversely affected by higher taxes on consumption. For the most part (e.g. in the US, Canada and Japan, with New Zealand as an exceptional case), this equity argument proved fatal to any push to dramatically increase reliance on consumption taxes, or to Governments that successfully did so. As outlined in Part 2, despite three attempts in Australia to shift taxation from income to consumption, the tax mix between them remains much as it was before the GST was introduced.

Outside the United States (which relies less on consumption taxes than almost all other OECD countries), the idea that income taxes should be completely replaced by taxes on consumption has lost favour. Optimal taxation research has also begun to question the notion that this is a sure path to improved economic efficiency and growth.

Forty years after the UK Institute for Fiscal Studies’ Meade Report advocated replacing income taxes with a progressive expenditure tax, the same organisation reviewed the arguments for taxing income and consumption. The Mirrlees Review still favoured expenditure taxes over income tax, but it drew a distinction between different kinds of income – the ‘normal rate of return’ and ‘economic rents’ (see discussion below) – and only proposed to exempt the former from taxation. The Institute commissioned Banks and Diamond to evaluate the arguments for and against taxing investment income. Contrary to the overall thrust of the review’s proposals, they found that the case for complete removal of taxes on investment income was weak. Research studies supporting this view used over-simplified assumptions (for example that capital is perfectly mobile). They concluded that while the case for taxing investment income at the same rates as wages was weak, it should still be taxed.

Back in Australia, a similar critique was made by Apps of a report by KPMG for the ‘Henry Review’ which estimated the economic cost of different taxes. She argued that the model used in this report overestimated the impact of the Australian income tax on the supply of labour (compared with that of taxes on consumption) because it assumed that all households had a single wage earner who increased his working hours in direct proportion to increases in his after-tax wage. The fact that women on lower incomes were more responsive to the costs of paid employment than men on higher incomes did not feature in the model. Yet they would be more adversely affected by a shift towards taxing consumption.

Similarly, some economic models assume that capital is perfectly mobile. This leads to the conclusion that a small open economy cannot sustain a tax on company income. Yet if this key assumption is relaxed, the results look different. In his summary of this research, Auerbach refers to:

‘possible outcomes ranging from capital still bearing a large share of the [company income] tax (Gravelle & Smetters 2001) to most of the tax being shifted to labour (Harberger 2008).’

As the 12th largest, Australia’s economy is hardly ‘small’. Our economy has always relied on foreign investment, but it also relies on domestic savings. Around two thirds of equity in Australian companies is owned by local investors. Company income tax revenue has taken a hit recently with the fading of the resources boom, but it remains higher (in proportion to GDP) than its average level in the 1980s and 1990s.

The challenge for income tax advocates is that the growing reach of multinational corporations and capital markets, and innovations in financial markets and information technology, are easing constraints on the mobility of capital and making it harder to follow the money trail. International capital is moving into black holes and ‘bermuda triangles’ where no national tax administration can reach it. This suggests it will become harder to tax investment incomes, especially those accruing to foreign investors. A key part of the solution is to strengthen international cooperation on tax and close off the worst abuses, but this won’t fully solve the underlying problem.

The trojan horse inside our income tax system

While the battle of ideas raged outside, the income tax appeared to be safe inside its citidel. Yet its rival, the expenditure tax, was already concealed within. Recall that the main difference between income and expenditure taxes is the treatment of investment. The tax treatment of many investments is closer to expenditure tax principles: there is either a deduction for new investment, or investment income is fully or partly exempted from tax. The table below ranks the main investment assets in Australia and compares their tax treatment.

Tax treatment of major investment vehicles (2010)

| Asset type | % of of all household assets | Tax treatment |

| Own home |

43% |

Taxed on purchase, capital gains and imputed rents exempt (expenditure tax) |

| Superannuation |

15% |

Contributions & fund earnings partly taxed with deductions for new contributions, benefits exempt (hybrid tax) |

| Investment property |

15% |

Rent fully taxed, capital gains partly taxed (hybrid tax) |

| Other financial assets (e.g. shares and bank deposits) |

7% |

Bank interest fully taxed (income tax);

Share dividends fully taxed & capital gains partly taxed (hybrid tax) |

| Own business |

5% |

Profits fully taxed, capital gains on business assets partly taxed (hybrid) |

We can see from this that investment income derived from over 40% of household wealth (capital gains and imputed rents from owner-occupied homes) is untaxed while income from at least another 40% is only partly taxed (mainly because capital gains are taxed a half the standard rate and only when the asset is sold – if at all).

Slemrod estimated that the effective tax rate on all investment income in the US was just 14-24% in 2002.

‘Calling a tax system an income tax or a consumption tax does not make it so. This is certainly true of the U.S. income tax system, which has long been recognised as a hybrid of an income and consumption tax, with elements that do not fit naturally into either pure system.’ Gordon et al, 2003

All income is not equal

Even the difference between ‘pure’ versions of income and expenditure taxes is not as stark as once believed. If we break investment income down into four component parts, it turns out that two of the four are taxed the same under income and expenditure taxes. The key difference is that only an income tax taxes the ‘normal’ or ‘risk free’ rate of return on investments, which is roughly equivalent to the Government bond rate.

Tax treatment of different components of income

| Investment income component | Income tax treatment | Expenditure tax treatment |

| Inflation component | Not taxed | Not taxed |

| Risk free or ‘normal’ returns | Taxed | Not taxed |

| Above-normal returns from risk | Not taxed | Not taxed |

| Above-normal returns from economic rents | Taxed | Partly taxed |

Part of the value of annual income flows from an investment such as a bank account is offset by inflation in the price of goods and services. Since this does not represent a gain in spending power, a ‘pure’ income tax should adjust investment income downwards for the effects of inflation. This was advocated by the Mathews report in Australia in the 1970s and implemented in our first tax on capital gains in 1985 (though not for other forms of investment income). So this ‘inflation’ component of investment income is not taxed under either a pure income or expenditure tax.

A second component of income is the ‘risk free’ or ‘normal’ rate of return which is also called the ‘reward for waiting’. Borrowers must usually offer a rate of return above inflation to attract investment; otherwise there would be little incentive for people to defer consumption. The minimum rate required is the ‘risk free’ rate, which applies to ‘safe’ investments such as Government bonds. This component of investment income is taxed by an income tax but not by an expenditure tax.

The third component is the extra (‘above normal’) return from risk. Riskier investments are more likely to make losses which attract income tax deductions (a pure income tax allows unlimited deductions for losses). This means that the extra or ‘above normal’ returns from risky investments are not in effect taxed under a pure income tax (and nor are they by an expenditure tax).

The fourth component of investment income is above-normal returns from economic rents. These arise where a business occupies a monopoly position in a market (as many believe the ‘big four’ banks occupy in Australia) or through scarcity in the supply of ‘immobile’ factors such as land or mineral resources. Where economic rents exist, returns are higher regardless of risk. Taxes on locally-specific economic rents, such as those arising from the exploitation of scarce mineral resources, are not a drag on economic growth because they remain an attractive investment proposition despite a tax on above-normal profits.

The economic rent component of profits is taxed under an income tax, but it may also be taxed under an expenditure tax. This is because even if new investment is fully deducted from tax (as it is with expenditure tax treatment) this concession is less valuable than the ‘super profits’ that can be obtained from economic rents. An important exception is the taxation of economic rents that accrue to foreign investors. In the absence of a domestic tax on company profits or on specific economic rents (such as those relating to mineral resources), these rents might escape tax in the source country (the country where the profits are made).

Of course, key elements of our income tax are either more or less generous than the ‘pure’ version. But these distinctions between different kinds of income are still important for tax policy. There is a strong case for taxing income derived from economic rents, whether directly or through company income taxes. On the other hand there is a strong case for taxing investments generally at lower rates than wages to take account of the impact of inflation on investment returns.

New ideas in tax reform

These more nuanced views of income and how it is taxed point to the real battle being fought within the income tax itself, over such issues as deductions for investment expenses, the treatment of capital gains, and tax breaks for long term saving. The set piece duels between the ideal of comprehensive income taxation and its expenditure tax rival have burnt up a great deal of political capital with limited effect, and may have distracted us from the main game.

These new (and not so new) understandings of taxation suggest that advocates of a progressive tax system should turn their attention to reforms of the income tax which:

- tax investment income more consistently, but at lower rates than wages (especially for long-term savings and foreign investment);

- target economic rents;

- take account of the impacts of tax on workforce participation by different groups, (especially low-paid women).

Another key problem to be solved (worthy of a separate blog) is the way the income tax interacts with the social security system. Income tests, together with the income tax, impose higher effective tax rates on low income earners. This problem can only be avoided entirely if social security payments are paid to everyone (as ‘demogrants’), and gradually clawed back above a high tax free threshold (e.g. through the tax system). In a revenue neutral reform, this would greatly increase tax rates on middle income earners (since the cost of semi-universal social security payments is too great to be borne by high income earners alone). In Australia these problems are sensibly addressed, but not solved, by income-testing income support payments for adults relatively strictly, and payments for children less so.

I’ll conclude with comments on some of the best reform ideas informed by this new thinking, including income taxes targeting economic rents, north European dual income tax models, wealth taxes, and the Henry Review proposals which draw upon all of these.

(1) Taxing economic rents

The basic approach to taxing economic rents is to tax profits minus an allowance for the risk free or ‘normal’ component of investment returns, on the assumption that the difference consists mainly of the proceeds of economic rents. This ‘residual’ profit is then taxed at a higher rate. This tax on ‘super-profits’ could be applied in conjunction with a standard company income tax (usually in industries where rents are likely to comprise the majority of investment income), or it could replace the corporate income tax altogether. In the latter case, the company income tax would be replaced, in effect, with a tax on corporate expenditure (this is proposed by the Mirrlees Review). The idea is to shift taxation away from investments that might be discouraged by tax towards those which are more likely to be indifferent to it.

A good example of an industry specific tax on rents is a mineral resource rent tax. To the extent that mineral resources are scarce and geographically immobile, they are likely to yield ‘above normal’ profits and taxing them in the source country is unlikely to discourage investment. The original idea for a resource rent tax came from Brown in the 1940s. Under his formula, expenses associated with exploration and extraction would be fully and immediately deductible and profits taxed well above the standard company income tax rate. In effect, the Government, as the owner of mineral resources, would join the investor as a silent partner, sharing the risk should a project fail and the returns if it succeeds. Ideally, this would replace royalties for the extraction of mineral wealth (based on the quantity extracted), which are more likely to discourage marginal investments and yield less revenue for Governments in the long run.

One problem with this ‘pure’ Brown tax is the long delay in collecting public revenue from mining projects (and the attendant tax avoidance opportunities). Indeed, there may be an initial revenue loss from the up-front deductions for exploration and other costs. To deal with this problem, mineral resources taxes such as the Norwegian one, and the Resource Rent Tax proposed in the Henry Report, required miners to carry forward these expenses and offset them against future income. If the project made a loss, any remaining expenses would be refunded. In return for the deferral of deductions for investment, these resource rent taxes only taxed profits above the ‘normal’ rate of return (often proxied by the public bond rate). One problem with this approach is that tax revenues would take a hit from loss-making projects in the aftermath of economic downturns – without any clear benefit to the ‘real’ economy. Nevertheless, a well designed resource rent tax is likely to raise more revenue than royalty payments, with less distortion of investment. Australia still has a Petroleum Resource Rent Tax on offshore oil mines.

In theory a similar result could be obtained across all sectors of the economy by deducting ‘normal’ returns from company income before taxing it, and taxing the remaining profits at a higher rate. In one prominent corporate income tax reform proposal, this ‘deduction’ is called an Allowance for Corporate Equity (ACE). The basic idea is that a company’s income tax is reduced by a percentage of shareholder equity in the company equivalent to the normal rate of return. Companies with low profits relative to investment assets would gain at the expense of those with higher profits (at least some of which are assumed to come from economic rents).

The case for taxing economic rents seems to be straightforward – public revenue is collected with less disruption of investment than from traditional company income taxes or mining royalties. If, however, taxation of economic rents replaced company income tax this would narrow the tax base since the normal rate of return would be exempt from tax. Taxing economic rents alone is equivalent, in principle, to replacing the personal income tax with a tax on expenditure (as discussed previously).

This raises some difficult questions: Would such a system raise the same public revenue without a much higher tax rate? Or would it reduce taxes on corporate income and make it harder to tax personal income, given the cross overs between the two sectors? Could a single country introduce such system and what would be the transition costs? The Henry Report raised the ACE as an option for the future but did not advocate it, opting instead for an industry-specific approach in the form of a minerals resources rent tax.

In the meantime, our company income tax captured – however imperfectly – a share of the income from economic rents during the mining boom at little cost to economic growth – but that revenue bonanza wasn’t going to last forever.

(2) Dual income taxes

While the Anglophone countries debated taxing investment income less, the high-taxing northern Europeans – under pressure from the easing of restrictions on capital movements across Europe – went ahead and did it.

From the 1990s on, the Scandinavian countries and Holland have formalised a previously implied distinction in their tax systems between income taxes on wages and investments. The logic of these dual income tax systems was that wages would continue to be taxed at progressive rates but investment income would be taxed at a lower rate, identical to the company income tax rate. This was a compromise between comprehensive income taxation and an expenditure tax (under which the tax rate for investment income is set at zero).

As described in an ACOSS Paper on personal income tax, the income tax system would be split into two parts: wages and investment income.

Dual income tax systems in Nordic countries (2004)

| Norway | Finland | Sweden | Denmark | |

| Tax rate for earnings | 28-48% | 29-52% | 32-57% | 38-59% |

| Tax rate for investments | 28% | 29% | 30% | 28/43% |

| Company tax rate | 28% | 29% | 28% | 30% |

| Offset of investment losses | Within 1st tax bracket only | Tax credit | Tax credit | Within 1st and 2nd brackets only |

| Net wealth tax | 0.9-1.1% | 0.9% | 1.5% | None |

An important feature of dual income tax systems is that deductions against one form of income (e.g. investments) against the other (e.g. wages) are restricted. This had a surprising impact on public revenues when Sweden established a dual income tax system in the midst of a deep recession in 1991. Despite the lowering of tax rates for much investment income, revenues rose substantially. More revenue was gained from denying deductions to home owners and property investors than was lost from the lower tax rates on investments.

An important benefit of the dual income tax is that it gives policy makers the flexibility to respond to downward pressures on tax rates on investment without undermining the progressivity of the tax on wages. This is balanced by some desirable elements of rigidity: tax rates applied to most investments are more consistent and the investment income tax rate is ‘anchored’ at the first step in the tax scale for wages (see table above). This is important for both equity and acceptability reasons. It means that high-income investors do not pay tax at rates that are lower than typical workers.

Dual income taxes have been criticised on equity grounds for not taxing all forms of income consistently. As shown above, the reality is that effective tax rates for most investments in Australia are already well below the standard marginal rates (especially for owner occupied homes and capital gains on other investments). If we abandoned the quest for a uniform comprehensive income tax and introduced a dual income tax, it would in a sense formalise the status quo, except that that investment income taxes would be more consistent and less distorting. To the extent that this results in higher tax rates on capital gains it would improve equity as these are heavily concentrated among the top 10% of income earners in most countries. Another bonus is that ‘negative gearing’ strategies would no longer be viable.

One problem from an equity standpoint is that low-income investors would pay tax at the same rate as high income earners. In the absence of a tax free threshold on investment income, this would bring many retired people on modest incomes into the tax net for the first time.

The main practical weakness of dual income tax system is the difficulty in drawing clear distinctions between labour and investment income, especially when labour is supplied through a private company. Scandinavian countries deal with this problem by taxing an implied return from small business assets at the (lower) investment income tax rate, and any remaining income at the (higher) tax rates for wages.

(3) Taxes on wealth

The defining feature of income taxation is that it taxes the accumulation of wealth (whereas consumption taxes tax the dissipation of wealth). An indirect way to achieve the same end is to tax the stock of wealth itself.

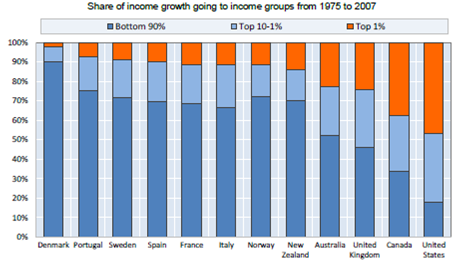

Since wealth is much more unequally distributed than income (the top 10% of Australian households by wealth holds roughly half of all wealth while the top 10% by income have roughly a quarter of all income), an effective wealth tax is likely to have a stronger inequality-reducing impact.

In Australia over the last 30 years, the top 10% of income-earners received around half of all increases in private income while the top 1% gained more than 20%. Taxes on wealth are another policy tool to offset this trend.

Annual wealth taxes – at low rates above a high tax-free threshold, and with owner occupied housing exempted – exist in three OECD countries. Their main weakness (as with taxes on investment income) is that to the extent that they tax mobile factors the revenue base could slip away. Broad-based wealth taxes in most countries that previously used them were easily avoided, and collected little revenue at relatively high cost (including annual valuation of assets).

Recognising the ‘mobility’ problem, Picketty advocates a modest broad-based international tax on wealth holdings, at progressive rates above a high threshold. His motive is to avoid the entrenchment and growth of wealth and income inequality, especially at the very top (1%) of the distribution. A wealth tax is easier said than done in a global context, but it could be an future option for international federations, especially Europe.

The ‘mobile wealth’ problem does not arise with immobile factors such as land. A well designed land tax is not only hard to avoid, it encourages the efficient use of land. Since it is tied to a specific location, land tax is an ideal tax base for Local or State Governments. Replacing taxes on housing transactions such as Stamp Duties with a modest land tax with minimal exemptions would improve the efficiency of property markets.

The tax base for taxes on estates or inheritance is transfers of wealth rather than the overall stock of wealth held by an individual. Unusually, these taxes attract ‘bipartisan’ support from income and consumption tax advocates. Inheritances would be captured under a comprehensive income tax. Consistent advocates of expenditure taxation argue that estates or inheritances should be taxed, on equity grounds, if income taxes were replaced by an expenditure tax. They are among the most equitable and economically efficient taxes. A tax on a windfall gain (or an estate whose final value is not known in advance) is unlikely to distort investment decisions, and it should encourage workforce participation to the extent that the beneficiaries are close to retirement and the windfall allows them to retire earlier. Around two thirds of OECD countries have estate or inheritance taxes. Australia did until the 1970s when they were wiped out by interstate tax competition.

Apart from their unpopularity, the main challenge for a tax on wealth transfers is stemming avoidance through such devices as gifts and private trusts, so that they fall on people with substantial wealth rather than those lacking the wherewithal to avoid them.

An interesting variation on wealth taxation is the use of wealth as a proxy for income. The Netherlands replaced its income tax on interest bearing accounts, shares and investment property with a tax on a (low) deemed rate of return on investment assets (owner occupied homes and small business assets were exempted). The idea was that it would be easier to measure (and capture) wealth than the income derived from it, and that such a tax would encourage its efficient use (since any income above the deemed rate of return is not taxed). Australian pensioners will recognise this idea – a ‘deemed rate of return’ on investments is used in the pension income test. Aside from its potential complexity, one disadvantage of this approach is that economic rents would not be taxed. Indeed, ‘deeming’ moves in the opposite direction to tax reforms which aim to tax rents but not normal rate of return.

(4) The Henry Report

I’ll end this series at the best place to begin a serious discussion of tax reform in Australia: the Henry Report. This major review of the Australian tax system undertaken by an expert panel chaired by the then Treasury Secretary, Ken Henry, sat somewhere in between the comprehensive, academic-led Mirrlees Review in the UK and the more short-term oriented, politically endorsed Taxation Working Group review in New Zealand.

The Henry Report pitched its reform proposals to the medium term (so I’ll ignore the short term responses of the major political parties – this is a longer game). It identified a number of challenges including revenue adequacy as the population ages, the internationalisation of economies spurred by technological innovation, distortions in the system that discourage investment or workforce participation and undermine housing affordability, and to strengthen equity in the income tax and transfer system.

Critics argue the Henry Report lacks a coherent reform narrative or framework, based on ‘ideals’ such as comprehensive income or expenditure taxation. Yet the outline of a framework is there, just below the surface. Its first recommendation is that:

‘Revenue raising should be concentrated on four robust and efficient broad-based taxes:

-

-

personal income, assessed on a more comprehensive base;

-

business income, designed to support economic growth;

-

economic rents from natural resources and land; and

-

private consumption.

-

We can see already that the Review Panel favoured an income tax that taxed different kinds of income more consistently, but mindful of the optimal taxation literature it did not advocate uniform taxation of investment and labour income. Its reform framework for income taxation is closer to the dual income tax model, or perhaps a ‘triple’ income tax comprising:

- Progressive taxation of wages;

- Taxation of income from shorter-term savings vehicles (including interest, dividends, and rent) at a 40% discount off marginal tax rates on wages;

- More concessional tax treatment for the two main longer-term savings vehicles (the current expenditure tax treatment for owner occupied housing, and a capped rebate for saving through superannuation).

The idea is to tax investment income at lower, progressive rates than wages (though less progressive than the present system due to a proposed flattening of the tax scale for wages, the economic benefits of which are not demonstrated). The proposed 40% discount is borrowed from the current tax treatment of personal capital gains, which attract a 50% discount off marginal personal tax rates. The 40% discount is a ‘rough and ready’ adjustment for the effects of inflation on investment income.

Under the proposed income tax system, taxes on capital gains would rise while taxes on interest and rents would fall, creating a more level playing field. While the proposed progressive tax rates for investment income are on the face of it more equitable than the flat-rate investment taxes in Northern Europe, there is no clear logic to the 40% discount. There is a risk that the discount would be ‘bargained upwards’ through the political process. In its response to the Report, the then Government proposed to increase the discount to 50%, albeit with a cap on the level of investment income to which it would apply. Alternatives to the proposed 40% discount include an explicit discount for inflation (one that varies with the inflation rate, which of course is now very low) or a variant of the northern European system with a tax free threshold for all investment income together with a flat tax rate ‘anchored’ in the marginal tax rate of a typical middle income wage-earner.

The exemption of owner occupied housing is politically and fiscally sensible. If Capital Gains Tax was extended to the main residence it would probably be limited to a small minority of home-owners, and home buyers should arguably be entitled to claim deductions for mortgage interest, at far greater cost to the fisc.

Special treatment for long term saving through superannuation is also desirable, since the impact of both inflation and income taxes on savings compounds over time. The review proposes fairer and more efficient tax breaks for saving through superannuation, including a capped rebate similar to proposals advanced for many years by ACOSS.

On the indirect tax side, the Report advocated the replacement of inefficient State taxes on business inputs and transactions (mainly Stamp Duties) and a broadening of the State Land Tax base to include owner occupied housing.

Its company and business income tax reforms focus on ‘supporting economic growth’. Here a trade-off is proposed between higher taxation of mining resource rents and the removal of some business tax concessions, and a lower company tax rate (from 30% to 25%), which is the ‘average rate for small to medium OECD economies ‘. The Review bought the argument that international capital is becoming more mobile and sensitive to tax, but wished to avoid a ‘race to the bottom in company income tax rates’ of the kind that created speculative investment booms in Ireland and Iceland. The quantity of investment matters, but so does its quality. Once again, this approach is more consistent with the Dual Income Tax model (with company income still subject to tax but at a lower rate) than the expenditure tax proposals of the Mirrlees Review. The transfer of resources from a booming mining sector to other industries (via a lower company tax rate) was also designed to aid Australia’s economic adjustment to the mining boom (since the high dollar was strangling other industries).

The Government’s ‘riding orders’ to the Panel to avoid discussion of the GST or taxation of superannuation benefit payments limited the scope of the Review. On the other hand, the state of media and public debate on taxation in Australia is such that if the Report had advocated a higher GST (or, for example, the introduction of an inheritance tax), none of the other recommendations would have been publicly discussed. The Review’s ‘core’ proposals as outlined above are arguably more important.

There were gestures in the direction of expenditure tax treatment of business income: the ACE was given a positive review (but not recommended for now) and there was a suggestion that State Payroll Taxes be replaced by a business cash-flow tax. Here the Review came perilously close to advocating an extension of broad based taxes on consumption, though the distributional impact of such a move is not clear since Payroll Tax already falls mainly on wages and consumer prices. As discussed in Part 2, replacing an inefficient tax on consumption with a more efficient one is not necessarily regressive.

As discussed above, the implications of such proposals for the future of personal income taxation are unclear. But rather than argue for ‘fundamental tax reform’ of the kind long advocated in the US (a major shift from taxing income to taxing expenditure) the Review Panel was content to wait for the dust to settle on the research evidence, and also the practicality, of such a move, noting that ‘a business level expenditure tax could suit Australia in the future.‘

The Henry Report, like the northern European Dual Income Tax model, is a working compromise between the old ideals of comprehensive taxation of income and expenditure, a bridge between the existing ‘mess’ (as Freebairn puts it) and a more coherent system. The proposals aren’t perfect, but that’s how tax reform works.

Concluding comment

Writing this three part ‘brief history of tax’ was a bit like walking through a hall of mirrors. The same passage looks different each time we walk through. In Part 1, the income tax was king and the main goal of reform was to tax income as uniformly and comprehensively as possible. Things looked different in Part 2 when viewed from the perspective of the ‘clash of the titans’ between two idealised tax systems: comprehensive income and expenditure. It turned out that the big difference between them is timing – whether we should tax returns from investment now or later. Still, this is an important distinction especially from an equity point of view, and that’s why consumption taxes (despite the vital contribution the make to efficient revenue raising) have not gained the upper hand.

In Part 3 we took a walk inside the income tax system while the champions slugged it out beyond the walls. The king is now not what he seemed to be. Our income tax system has expenditure taxes hidden within. It’s no longer obvious that the path to reform leads to either a pure comprehensive income tax or its replacement by a consumption tax.

The most important battles for reform lie within the income tax itself. Some are familiar, such as the unceasing effort to rid the system of unproductive tax shelters (Sisyphus comes to mind here). Others are new, including efforts to seek out and tax economic rents. I hope this series helps equip a few people to fight them.