‘The tax code, once you get to know it, embodies all of the essence of life: greed, politics, power, goodness, charity. Everything’s in there.’ Sheldon Cohen, Former Commissioner of the US Internal Revenue Service.

Tax reform is back on the agenda. Since those who fail to study history risk repeating it (and I was involved in the latter-day history of tax reform) I’m writing this 3 part series as a guide for those involved in the next phase. Part 1 dealt with the dominant tax of the second half the 20th century – personal income tax. This part describes the intellectual and political contest between taxing income and consumption over the last four decades: a clash of tax titans.

Readers with an interest in detail can check out the references in Part 1 of this blog. In addition, good summaries of the arguments for and against a switch from taxing income to taxing consumption are provided by Brooks, Auerbach, and Henry. Those wanting to keep up with current Australian tax debates should visit the Tax Watch site.

Re-capping the income tax story

By the 1970s the income tax was ‘king’. Personal and company income taxes raised the majority of public revenue in Australia. Income tax was a key tool for redistributing resources from those with the greatest ability to pay – those with higher incomes – towards those with the least. Elite and public support for income tax faded during the 70s and 80s for a complex set of reasons: inflation was moving ordinary wage earners into higher tax brackets while high income earners could readily avoid paying tax. At the elite level, redistribution was out of favour as wealthy nations grappled with the failure of the post-war economic model to deliver steady growth in living standards. The neoliberal view – that these problems could only be resolved if constraints on the free operation of markets were removed – gained traction.

One of the constraints identified at this time was the income tax system, which distorted saving and investment decisions (these were too often made for tax reasons rather than to achieve the best returns) and discouraged workforce participation. These economic efficiency concerns carried more weight in tough economic times.

They did not necessarily conflict with equity concerns. Neoliberal economists were among the strongest supporters of a comprehensive income tax – one which taxed all forms of earned income and investments consistently. That meant the removal of tax shelters and loopholes which mainly benefited people with high incomes. The major Australian tax reviews in this period advocated the perfection of the income tax model, not its abandonment.

Yet there was an alternative to reconstructing the income tax. The Hawke Government’s 1984 ‘Draft White Paper’ on Tax Reform advanced three options: Option A cut income tax rates by closing tax shelters, Option B added to this reform the replacement of a ramshackle set of federal sales taxes with a broad based tax on consumption. Option C went a step further by increasing the proposed consumption tax to pay for deeper income tax cuts. Option B was an internal clean-up of consumption taxes. Option C had the more ambitious aim of changing the mix of taxation from income to consumption, or expenditure.

While it only came into prominence in Australian public debate in the 1980s, the idea that a broad based tax on consumption was superior to an income tax had deep historical roots. At its core, this was an argument about the tax treatment of saving and investment.

The expenditure tax alternative

‘The Equality of Imposition consisteth rather in the Equality of that which is consumed, than of the riches of the persons that consume the same. For what reason is there, that he which laboureth much, and sparing the fruits of his labour, consumeth little, should be more charged, than he that living idlely getteth little, and spendeth all he gets: seeing the one hath no more protection from the Commonwealth than the other? But when the Impositions are layd upon those things which men consume, every man payeth Equally for what he useth: Nor is the Common-wealth defrauded by the luxurious waste of private men.’ Hobbes Leviathan Ch. XXX. (from Kaldor, see below)

Hobbes’ 17th century ‘moral’ argument for taxing expenditure instead of income seems curious today since the purpose of saving is to make room for more spending later on. If we all ‘consumed little’ the economy would grind to a halt.

The modern-day case for taxing expenditure instead of income was first advanced by an American economist, Irving Fisher in 1942. This argument would rage among tax experts, out of earshot of the general public, for the next half century and beyond.

Fisher’s case for a tax on expenditure seems far removed from Australian public debate over sales taxes like the GST. Yet it is about the same issue: how savings should be taxed.

Just as the top income tax rate in the US reached its zenith (a top marginal rate of 80%) during World War 2, Fisher proposed an alternative, the spendings tax. Fisher’s main objection to the income tax was that it unfairly penalised saving since (as I pointed out in Part 1) it taxed investment income as well as wages and this amounted to ‘double taxation’ of savings. His solution was to remove the taxation of investment income by taxing cash-flows instead of income.

To simplify, the tax base would be the difference between cash on hand at the beginning of the year together with wages and cash income from investments accrued during the year, and cash remaining at the end of the year. The difference was the amount spent during the year. His proposed ‘spendings tax’ was actually a tax on consumption (income minus saving), but unlike sales taxes it would be raised directly from the taxpayer rather than indirectly from retailers (who then pass it on to the consumer).

The above quote from Hobbes was the opening page of Nicholas Kaldor’s book ‘An expenditure Tax’, published in 1955. Kaldor brought the idea of replacing the income tax with a tax on expenditure to the United Kingdom. This idea gained greater prominence after the release in 1978 of a landmark report by the Institute for Fiscal Studies, the ‘Structure and reform of direct taxation’. The report, prepared by an expert committee headed by James Meade, argued for replacement of the income tax with a ‘progressive expenditure tax’:

‘A progressive expenditure tax is the one form of tax which could have the political appeal of encouraging enterprise and economic development and at the same time heavily taxing high levels of consumption expenditure which at present, if it is financed out of capital, goes untaxed.’ p33

Equity and efficiency arguments

These were bold claims, and they conflicted with the common sense view that taxes on consumption were regressive. Meade and other expenditure tax advocates were not arguing the community should accept a less equitable tax system in order to promote economic growth. They were saying we could have our proverbial cake and eat it, too.

The equity case for progressive income taxes rests on two main arguments: that they tax individuals directly at progressive marginal rates and that income is a better measure of the resources available to people than consumption.

By contrast, existing consumption taxes were imposed ‘indirectly’ as sales taxes on retailers and not ‘directly’ on consumers. This meant that they ignored differences the overall level of consumption among people of different means. It was not possible to tax consumption at progressive rates using a sales tax (this could only be done imprecisely by taxing luxuries at higher rates).

Fisher, Kaldor, and Meade’s solution to this problem was a ‘direct expenditure tax’. Instead of taxing consumers indirectly via retailers, they would be taxed directly on their consumption. This could be done by converting the income tax into a tax on spending. The key was to remove from taxation that part of income which is saved. Meade described a number of ways in which this could be achieved. One option was to deduct from tax any amounts saved during the year (e.g. outlays on new investments or repayment of loans). Another option was to exempt investment income (such as interest and dividends) from tax. These changes would be coupled with the taxation of any reduction in savings as they were drawn down to be spent (as superannuation benefit payments were previously taxed in Australia). Since each individual would be taxed directly on their income minus amounts saved, tax could still be levied at progressive rates.

This focussed debate on the real difference between taxing income and consumption – the tax treatment of savings. The equity case for income taxes rests on the idea that income or ‘spending power’ is a better measure of ‘ability to pay’ than expenditure because the ability to save and invest part of our income enlarges life choices (for example, to improve housing security by buying a home). Consumption tax advocates put the contrary view: that spending is a better measure of access to resources and that by taxing the returns from saving, an income tax favours current spending and penalises future spending.

A related argument is whether ‘ability to pay’ is best measured each year, or across the life course. An annual measure favours income taxes (since income taxes impact less on people whose ability to save is constrained), whereas consumption tax advocates argue that their tax is fairer on a lifelong basis (since income must eventually be spent and it is best not to interfere with people’s choices to save and defer their spending). Of course, not all income is spent during our lifetimes: many people leave part of their wealth to the next generation. To deal with the equity objection that taxation of savings could thus be deferred indefinitely, consistent expenditure tax advocates (including Meade) argue for taxes on gifts and inheritances.

A key question from an equity point of view is whether people who are relatively well off derive more benefit from a tax system that allows them to defer taxation on income from their savings until they spend it.

Key issues from an economic efficiency point of view are which of these two tax bases have the least adverse impact on saving, investment, and workforce participation, with a minimum of distortion of decision-making in each of these areas.

I’ll deal with these issues in a separate blog: ‘Who’s the fairest (and most efficient) of them all?’ For now, let’s turn to how the clash of these two tax titans – income and consumption taxes – was resolved in Australia and other wealthy countries.

The tax mix hasn’t changed much at all

If we take a virtual trip to Cabarita Beach in northern NSW, we’ll find this sign:

‘Historic site: At this precise point, on the morning of December 12 1927, nothing of significance is known to have occurred.‘

The outcome of the argument over the optimal tax mix feels a bit like this.

On the face of it, 40 years of fierce intellectual and political argument over the ideal tax mix has had little impact on the balance between income and consumption taxes in wealthy countries. What it has achieved is a more nuanced view of the taxation of income and savings, informed by a substantial body of research.

The share of consumption taxes in public revenue of OECD countries (top line) fell during the 1970s and has been stable since. This is the result of two conflicting trends: a decline in customs duties and taxes on specific goods offset by a rise of broadly based ‘value added taxes’ such as Australia’s GST.

The revenue share of income taxes also remained stable, but this masked major changes in the composition of taxes on income.

The key change here over the last 40 years was a reduction in the share of personal income taxes (top line), offset by a rise in social security taxes (second line). These taxes, used in Europe and the US to finance social insurance payments, are usually raised at a flat rate.

This change, along with less progressive income tax rate scales, reduced the progressivity of income taxes. Interestingly (given arguments that company income taxes would be competed away), the share of corporate tax revenues (bottom line) remained stable, even rising in the 1990s.

Enduring differences in the tax mix among countries

There are enduring differences in the tax mix and revenue ‘take’ between the Anglophone countries and most of Europe. The Anglophone countries raise less tax overall but do so more progressively, with a greater reliance on progressive income taxes. Most European countries raise more revenue, but rely less on income taxes and more on consumption or social insurance taxes to do so.

As shown in an OECD analysis, these international differences reflect different strategies to redistribute income in European and Anglophone countries. Across northern and central Europe, generous social insurance payments for retirees, people with disabilities and unemployed people play a major role. These require much higher taxes, and European countries are more tolerant of less progressive tax systems as long as they raise the revenue needed for these and other social programs. Australia, the US and Canada have more parsimonious social security systems and their electorates are more sensitive to any reduction in the progressivity of the tax system. This reflects the Anglophone emphasis on ‘targeting’ of both benefits and taxes to achieve distributional gaols with smaller welfare systems.

An exception is New Zealand, where social security payments are low and Governments have reduced the progressivity of the tax system by cutting top marginal tax rates and increasing the GST. New Zealand Treasury analysis found that recent changes along these lines in 2010 had little impact on the real disposable incomes of households on less than $NZ20,000 but boosted those of households earning over $NZ200,000 by an average of almost 3%. Tax policy changes along these lines, together with radical deregulation of the labour market, have led to one of the largest increases in income inequality among OECD countries over the last 30 years, with the gini coefficient rising from 0.27 (well below the OECD average) to 0.33 (slightly above it).

What happened in other countries?

In Europe, the major change to consumption taxes since the 1970s was the increased use of broad-based Value Added Taxes (like our GST, these tax the increase in the value of a product at each stage of its production and sale, offset by refunds for the cost of inputs). But the replacement of narrowly based consumption taxes and customs duties with VATs was part of a European Union push to modernise and standardise consumption taxes. It was not an attempt to replace income taxes.

The introduction of VAT by the Thatcher Government in the UK followed this logic. The Meade Report was not well received by her Ministers, who were wary of his proposed gift and inheritance tax and believed an incremental approach to tax reform was more likely to succeed than replacing the income tax with a new tax on expenditure. Its main influence on tax policy in the UK was the introduction of tax relief for long-term saving (for example through Tax Exempt Savings Accounts or TESSAs).

There was little interest among countries with the greatest reliance on consumption taxes to increase it further. Instead, the push for taxing consumption more and income less came from a country where consumption taxes were low: the US. This idea was called was called ‘fundamental tax reform’ – and there was an air of fundamentalism about it:

‘I strongly believe that Congress should abolish the income tax system in its entirely and begin anew. A single rate consumption tax on goods and services is the fundamental change needed to spur economic growth and increase wages, saving and investment. Our intrusive tax system should be transformed to one that is fair, transparent and friendly to savings and investment. A sales tax would achieve these goals and allow us to abolish the IRS. Every dollar the American people earn would be theirs to save, spend or invest. They would not have to account for it or face intrusive audits. They could pass it along to loved ones without strings attached.’

Senator Lugar, January 20, 1999 press release.

Proposals to replace US income taxes with a federal consumption tax have not centred on sales taxes like the Australian GST, perhaps because the US States already have sales taxes of their own. In 1977 the US Treasury, in its ‘Blueprints for Basic Tax Reform‘, proposed a progressive expenditure tax similar to Meade’s proposal. This would have been levied at progressive rates, and would have replaced the federal income tax. It would have exempted income from investment and taxed withdrawals from savings accounts. Business would be taxed on cash flow rather than income. ‘Blueprints’ also raised an alternative option – a more comprehensive income tax – and this proposal (not the progressive expenditure tax) was the launch pad for the Reagan tax reform a decade later (discussed in Part 1 of this series).

‘Blueprints’ was followed in 1983 by the ‘flat tax’ proposed by Hall and Rabushka, a tax on business cash flows coupled with a flat tax on wages above an annual threshold. Not surprisingly, this was widely opposed on equity grounds with studies finding it would increase inequality in both the short and long term.

In 1985 Bradford proposed his ‘X Tax’. This was similar to the ‘flat tax’ except that wages would be taxed at progressive rates and business cash flow would be taxed at the top personal tax rate. The ‘X Tax’ was clearly more progressive than the ‘flat tax’ but as with other expenditure taxes, replacing the income tax with the ‘X Tax’ would have benefited those with the ability to save a large share of their income (who are generally relatively well-off), and devalued the savings of retirees.

The push to replace US federal income taxes with an expenditure tax has been spectacularly unsuccessful. In the absence of a federal sales tax, the US relies less on general sales taxes than virtually any other OECD country. As in the UK, the expenditure tax debate led to new tax breaks for long-term saving, but their impact on household saving levels is disputed.

Fundamental tax reformers in the US over-reached in trying to achieve the toughest goal in tax reform – introducing a completely new tax:

‘Replacing the entire income tax with a consumption tax would be a grand experiment of applying theory to a practical application that no other country in the world has chosen to undertake. Proponents of these plans must, therefore, overcome a significant hurdle – they must show that it is worthwhile to conduct this experiment on the world’s largest and most complex economy.’ (former) Assistant Secretary for Tax Policy, Les Samuels, June 7, 1995 testimony.

What happened in Australia?

The strongest push to raise taxes on consumption here came in 1984 with Treasurer Keating’s ‘Option C’. This would have replaced existing consumption taxes with a broad based consumption tax (GST) at 12.5%, enough to pay for substantial income tax cuts. While not opposed to a GST in principle, both ACOSS (representing the community sector) and the ACTU (representing unions) opposed a large consumption tax due to its impact on the cost of living, and equity. At the national tax summit, business representatives opposed all three options because they were not prepared to support the removal of income tax shelters in ‘Option A’ (which included a Capital Gains Tax and a Fringe Benefits Tax).

Once Prime Minister Hawke realised that none of the key sectors were prepared to support ‘Option C’, he pulled the plug. The income tax reforms in ‘Option A’ were introduced regardless, and used to pay for more modest income tax cuts. The business sector learnt its lesson: following the Tax Summit the CEOs of large businesses established the Business Council of Australia to help it formulate common policy positions to take to Government.

This left the consumption tax base in disarray. The Wholesale Sales Tax only taxed goods and not services, yet services were growing in economic importance. State excise taxes on petrol, alcohol and tobacco were later struck down by the High Court on constitutional grounds, and many of the other State indirect taxes, especially Stamp Duties, were widely regarded as economic inefficient. Along with the US, Australia was one of the few OECD countries without a broad based tax on consumption.

The next attempt to introduce one was a crazy-brave push from Opposition in 1993 by the Coalition Parties led by John Hewson. His ‘Fightback’ package would have progressively replaced industrial awards with individual contracts, abolished Medicare, placed time limits on unemployment benefits, and introduce a Goods and Services Tax. Coming after a recession when people craved economic security, ‘Fightback’ scared voters and the Labor Party won the election.

Hewson’s proposed GST rate was 15% and this would have funded a 30% reduction in income taxes as well as replacing existing consumption taxes (since the GST would have replaced State Payroll Taxes as well as the Wholesale Sales Tax, the proposed change in the tax mix towards consumption was not as large as ‘Option C’).

The Howard Government learnt its lesson from the ‘Fightback’ experience. Its attempt to introduce a GST started in 1996 with a two year period of public discussion over the state of the tax system and options for reform. This discussion was led by an unusual combination of business organisations (the Australian Chamber of Commerce and Industry and BCA) and the community sector (represented by ACOSS). In a departure from previous tax reform efforts, they agreed that the basis for reform should not be a change the mix of taxation between income and consumption. The goal was to broaden both of these tax bases by winding back shelters and exemptions. There was agreement between business and ACOSS that tax avoidance through private trusts should be curbed (as urged by then Tax Commissioner, Michael Carmody), that company car fringe benefits should be fully taxed, and that the consumption tax base should be broadened to services. ACOSS also sought a tightening of Capital Gains Tax and negative gearing arrangements, and reform of superannuation tax breaks. Business organisations wanted food included in any new consumption tax, but ACOSS opposed this since food was about a quarter of all expenditure by low income households.

Modelling conducted for ACOSS suggested that if a GST only replaced existing (narrower) consumption taxes, and food was exempted, the change would have little impact on household spending power, and could easily be compensated through modest benefit increases and tax cuts (not shown here). The impact on the distribution of spending power would have been negligible.

If reform along these lines were implemented, more robust revenue bases would be available for social programs and at least some of the community sector’s long standing proposals to remove income tax shelters would be implemented. Business would achieve the removal of ‘input taxes’ on the production of goods (Wholesale Sales Tax, bank duties, and possibly Payroll Tax). It was in the interest of both sectors that any broad tax on consumption was used for this purpose rather than to pay for income tax cuts – a change that was likely to be regressive.

To strengthen the tax base of State Governments and to make it more difficult for future Commonwealth Governments to raise the GST to finance income tax cuts, ACOSS proposed that all GST revenues be allocated to the States, and that unanimous State and Commonwealth Government agreement should be required to increase it or extend to items such as food or community services. This proposal was adopted. After two failed attempts to introduce a broad consumption tax, the Government knew it had to show the public that the new tax would be difficult to increase later on (even though this constraint was political rather than legislative). It was also aware of the States’ need for a more robust and efficient revenue base.

But the Government had other ideas on the tax mix. Recalling the experience of the Coalition Parties in 1993, when Keating offered the electorate almost the same income tax cuts as the Coalition without a GST, the Howard Government opted for a tax package with a 10% GST with no exemption for food, which would replace some existing sales taxes and pay for large income tax cuts. A crackdown on tax avoidance through private trusts (by taxing discretionary trusts as companies) was included in the package, but motor vehicle industry lobbying prevented the removal of tax breaks on company cars. Following the Australian tradition of animal names for tax reforms, it was called A New Tax System, or ANTS.

ACOSS rejected the Government’s tax proposals, and so did the Senate. Due to the inclusion of food in the tax base and the use of the GST to fund income tax cuts, the Government’s tax reform package would have been strongly regressive despite compensation for low income households (in any event, ACOSS regarded a heavy reliance on ‘compensation’ as too risky for these households). It did little to remove tax shelters that undermined equity as well as distorting investment decisions, and would have resulted in a one-off rise in the cost of living of around 2-4% for households on modest incomes.

Australian Democrat Senators negotiated a less inequitable reform package with the Government, in which fresh food was removed from the GST and the income tax cuts were pared back at the top end. These were sensible changes to improve its fairness and secure public support for reform, and research conducted for a Senate Inquiry into tax reform found that their impact on future economic growth would be minor. Regrettably, the revised package took no further steps to broaden the income tax base. Two thirds of the cost of removing fresh food from the GST was met by keeping regressive State indirect taxes slated for abolition.

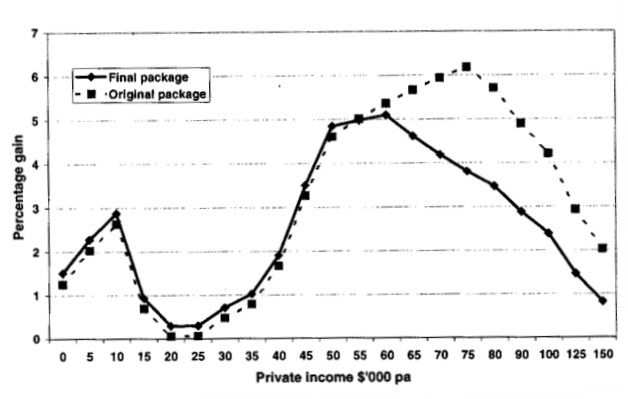

The result was a less regressive reform, but a regressive one none the less. This graph shows the results for singles without children. The reform boosted the incomes of most high income earners by around 3%, most middle incomes by around 2%, and most low income households by 0% to 3%. The removal of fresh food from the GST reduced the risk for low income households and the removal of top-end tax cuts reduced the gains for high income earners. Another positive outcome was that the food exemption and increases in family payments particularly benefited low income families – not shown here. (Note that the tax cuts and benefit increases cost more than the rise in consumption taxes, so most households gained in the short term at the expense of the fisc. It’s easy to create winners in this way)

The proposal to tax discretionary trusts as companies was not legislated up front as a condition for passage of the GST. Once the GST became law, the trust reforms withered on the vine. A subsequent business tax review argued for curbs to tax avoidance through private companies but at the last minute it also proposed a widening of the tax shelter for capital gains (by replacing inflation adjustment of capital gains with a halving of tax rates on nominal capital gains). ACOSS warned that this, together with the retention of negative gearing, would fuel the next speculative housing boom.

The outcome in Australia

After two failed attempts to modernise consumption taxes and shift the tax mix from income to consumption, the third attempt was successful. It increased the consumption tax share of overall public revenue by just under 2%.

Yet over the longer term, the share of consumption taxes in public revenue remained remarkably stable, returning after a decade to the pre-GST level of around 27%, compared with an OECD average of 33%.

Much has been made of the higher share of income taxes (including on companies) in Australian public revenues. In 2012 this was just over 60% compared with an OECD average just over 50%, when social security and payroll taxes are included. Australia’s income tax share of total revenue may be relatively high, but as the fifth-lowest taxing country in the OECD, our ratio of income taxes to GDP (16%) is close to average (15% including employee social security contributions). This is hardly unsustainable. The challenge now, with the federal budget in deficit and the looming costs of an ageing population, is to strengthen public revenue in a way that is both fair and economically efficient.

Conclusion

The 40 year battle between advocates of income and consumption taxes has improved the sophistication of tax policy discussion at the elite level. The tax treatment of saving and investment is now better understood, and policy is informed by decades of careful research. Yet the public is still wary of consumption taxes, and their intuition that these taxes are more regressive than income taxes is pretty accurate (see my next blog ‘The fairest of them all’).

A key problem for advocates of a shift towards taxing consumption is that while the impact of such a change on the distribution of income can be measured reasonably accurately (at least in a single year), its economic impact is harder to quantify. The stability of the tax mix in Australia and other countries suggests that the public have not bought the argument that we would be better off in the long run if we relied more on consumption taxes.

The clash of the titans has aroused passions on both sides, and this in itself has made tax reform more difficult. It may be time to move on.

Many of the economic benefits of a shift from taxing income to consumption could be achieved by reforming the income tax itself. This will be the topic of the final part of this series.

In the tax mix part of your blog you mention that the gst increased the share of tax by indirect taxes by 2%of GDP. I think that it should read just 2%. The gdp is irrelevant when discussing the share of tax or share of revenue.

Otherwise, a great read.

LikeLike

Thanks Joshua, And yep, that the increase in the share of consumption taxes in all revenue in 2000 was 2%. Regards

Peter

LikeLike