Publications

2025

Davidson, P and Hall, J (2025), Homes for living, not wealth creation: Tax and expenditure reforms to improve housing affordability and equity, ACOSS, Sydney

Deduct the losses, capitalise the gains:

how negative gearing works

Negative gearing arouses passions on both sides: about a third think people are making legitimate deductions, a third think it’s a rort, and a third don’t know. This blog, based on a recent ACOSS report, “Fuel on the fire”, takes a closer look.

In negative gearing strategies, investors borrow to buy an asset (such as a rental property), and structure the loan so that interest payments and other costs exceed income from rent. This investment ‘loss’ is then deducted from their other income, such as wages. On the face it, perfectly legitimate: the tax system allows people to deduct their expenses from their income and this is what they’re doing. The puzzle is why people deliberately make losses for many years on their investments. Even if they save on tax, aren’t they losing overall? The answer to this puzzle is the key to understanding how negative gearing works and whether or not it’s a legitimate feature of our income tax system.

How negative gearing works

To illustrate with an example (a simplification, not a real one):

“Ms Invest buys a rental property for $600K, with an annual rental return of $25K (around $500pw)

Her annual running costs (maintenance, agents fees, etc) are $10K

To maximise her borrowing capacity and take advantage of negative gearing arrangements, Ms Invest uses a more expensive ‘interest only’ loan, on which the bank gives her discretion to make higher or lower payments each year, so that the investment consistently makes a cash ‘loss’.

Now, say she borrows 80% of the value of the property (around $500K) and pays $25K a year in interest (5%).

So her annual expenses are $35K and income from rent is $25K: a cash ‘loss’ of $10K before tax.

Ms Invest deducts this $10K ‘loss’ against her wage of $150K (over half of geared property investors earn at least $100K, according to RBA research cited in the ACOSS Report).

Her marginal tax rate is 39% (including the Medicare Levy). So the tax saving from this deduction is around $4K. Taking this into account, she’s making an annual after-tax cash ‘loss’ of $6K a year ($10K – $4K). [there are other tax benefits like building depreciation but let’s set these aside to simplify things]

So why does she do it? The answer – and this is what really drives negatively geared property investments – is capital gain. That is, the increase in the value of the property each year which Ms Investor will cash in (or ‘realise’) when she eventually sells it. Until then, she can use it to reduce her income tax. When she does sell, only half the increase in the property’s value (the capital gain) is taxed. This ‘50% discount’ was introduced in 1999, just before negative gearing strategies really took off.

Let’s say the property increases in value by 5% a year – which is conservative in capital city property markets today. That’s $30K a year.

So instead of making an annual ‘loss’ of $10K before tax, she’s actually making a profit on the investment of $20K ($30K – $10K). After tax, her annual profit is $18K ($24K on the capital gain minus $6K on the other income and expenses). In effect, taking account of Capital Gains Tax and deductions for expenses, the annual tax rate on her investment is just 10% ($2K divided by $20K).

This is the problem with negative gearing: deductions are being claimed for investment ‘losses’ that aren’t really losses. Ms Invest is making cash ‘losses’ before she sells the property, but then profits when she sells it years later and makes a lightly taxed capital gain.

Solutions

There are three ways to fix this problem.

One option is to tax capital gains each year as they accrue (before the property is sold), at the same marginal tax rate at which the deductions are being claimed (in this case 39%). The problem with this is that Ms Invest might not have the cash-flow to pay this tax, and it would require an annual valuation of the property. This is not a practical option.

A second option, advanced by the Henry Report, is to reduce the tax discount for individual capital gains from 50% to 40% (so that 60% of gains are taxed), and then only allow investors to deduct 60% of their investment expenses. This ensures that gains and losses are at least taxed in the same way: 60% of capital gains are taxed and 60% of the associated losses are deductable (instead of 50% of the gains and 100% of the losses). The problem with this is that there’s still a timing advantage. Ms Invest can claim deductions for many years but is only taxed on the capital gain when the property is sold. As they say, time is money!

The third option deals with this problem by delaying the deductions. To stop people claiming deductions against investments which aren’t actually making losses, their investment ‘losses’ could no longer be deducted from their wages. Instead they would be ‘quarantined’ and carried forward to be deducted against future cash profits from the investment. If the property is not negatively geared, the expenses could still be deducted as they accrue, so nothing changes. If it is negatively geared, the deductions might be delayed a few years until the investment makes a cash profit (due to lower interest payments and higher rents). In extreme cases they might be delayed until the property is sold, in which case the investment expenses are deducted against the capital gains.

The idea is to ‘ring-fence’ income and losses from an investment so that gains and losses are treated in the same way (symmetrically). The deductions are not denied, they are delayed.

This is not a new idea. It was adopted by the Hawke Government in 1985 (and a mythology has emerged over its impact on rental property investment and rent levels, as explained in the ACOSS Report). Similar rules are in place in most wealthy countries including the United States and United Kingdom (see table).

The same principle is already applied in other areas of Australian tax and social security policy:

- Investment property losses cannot be deducted against other income in the income tests for social security and family payments.

- Trust losses are quarantined within the trust and cannot be offset against the income of the beneficiaries.

- Capital losses are quarantined and carried forward so that they can only be offset against capital gains.

- Some active business losses (e,g, hobby farms) are quarantined and cannot be deducted against the owner’s other income.

These quarantining rules are all designed to tackle a common problem: the tax treatment of investment income and expenses is lopsided. Investment income is taxed concessionally, so allowing unlimited deductions against other income (that’s taxed at ‘normal’ rates) threatens the integrity of the tax system. These rules were developed in response to real problems (rorting of the tax system and revenue leakage), not just theoretical ones.

In the case of negative gearing, the underlying problem is the tax treatment of capital gains. This problem extends well beyond rental property, to geared investment in shares (leveraged equities), agricultural schemes (like the ill-fated Timbercorp), racehorses and works of art – personal investments that mainly yield income in the form of capital gains. The same quarantining rules should apply to these investments.

As the ACOSS Report spells out, this is not just an equity and tax integrity problem: it blunts the efficiency of investment, and the economy. The tax system is encouraging people to borrow more than they otherwise would to punt on the capital gains in the property market. We’ve seen over the housing booms of the 80s and 00s what this does to housing costs and macro-economic stability. And Timbercorp is a case study of the harm that can come when people are encouraged to invest with tax deductions in mind rather than the quality of the investment.

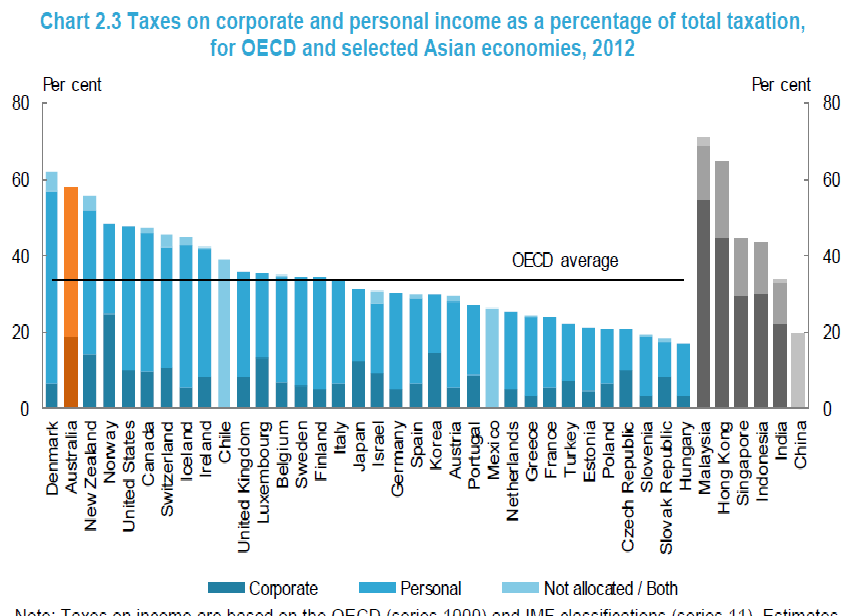

Reading the press you’d think a key message from the Govt’s Tax Discussion Paper is that Australia relies a lot more on income tax than other wealthy countries. Not so! Read the fine print and we find that 63% of public revenue in Oz comes from income and income-like taxes compared with 61% across the OECD.

What the Govt’s Tax Discussion Paper says about our reliance on income tax

When he released the Tax Discussion Paper at an ACOSS function last week (the one oddly titled “Rethink” – Rethink what? Most of the work was done in the Henry Report), Treasurer Joe Hockey repeated the hoary old argument that Australia relies too much on income taxes:

“Australia’s heavy reliance on income taxes may be unsustainable”

I pointed out in my last blog that the Discussion Paper found that personal income tax is no less efficient than the GST, though company income taxes detract more from economic growth.

But there’s another factual problem here: we don’t rely a lot more than other OECD countries on income taxes, when apples and compared with apples.

The claim that we rely heavily on personal and company income taxes is illustrated by this graph in the Report. It compares revenue from personal income and company taxes for all levels of Govt across the OECD. On this count, we’re second highest to Denmark (see yellow bar).

The Discussion Paper notes that:

“Australia relies more heavily on income taxes on company and individual income (often

termed ‘personal income tax’, including by the OECD) than other developed countries (Chart 2.3)

There’s a problem with this comparison. One of the things we have in common with Denmark is that we don’t levy social insurance taxes to pay for public pensions and unemployment benefits. Most OECD countries do. These are taxes on income, and should be included.

In its next graph, the Discussion Paper includes social insurance taxes, and also Payroll Taxes which have a similar purpose (Payroll Taxes are ultimately a tax on wages. They were introduced in Australia to finance Child Endowment). Here the story changes. We’re close to the middle (yellow bar); with 63% of public revenue coming from these taxes compared with 61% across the OECD.

The Discussion Paper notes that:

“Direct forms of taxation — individuals and corporate income taxes, compulsory social

security contributions plus payroll taxes — comprise around 63 per cent of taxation in

Australia. This compares to the OECD average for direct taxes of 61 per cent (Chart 2.4).”

Some argue that our Superannuation Guarantee should also be included, and that this would raise our reliance on income taxes overall. The trouble with that argument, as the Discussion Paper points out, is that:

“Australia’s compulsory superannuation system — the superannuation guarantee — is

sometimes equated to a social security tax. However, as it is paid directly into private

superannuation accounts (currently set at 9.5 per cent of an employee’s ordinary time

earnings) rather than to the government, it does not meet the definition of a tax.”

Put this together with the fact that Australia has low tax revenue overall (seventh lowest in the OECD, see the yellow bar), and our overall reliance on income taxes doesn’t look so high.

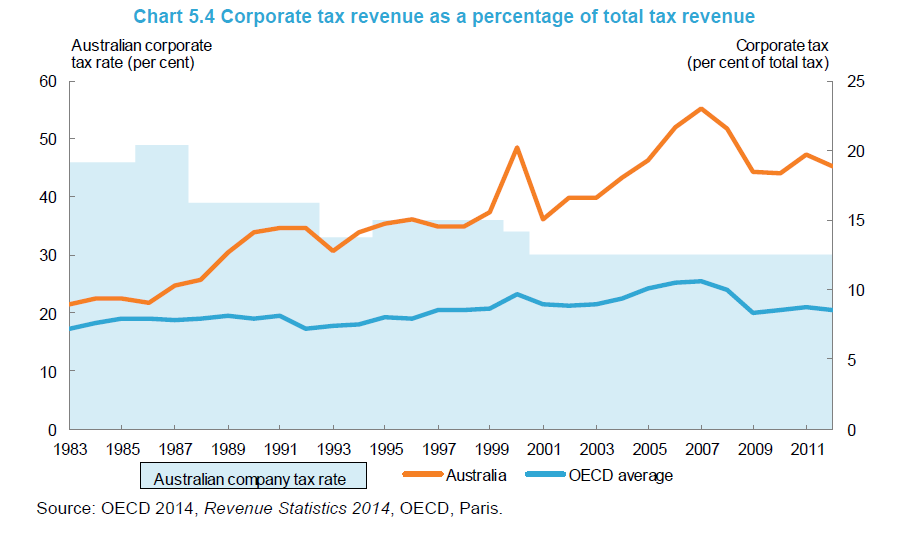

Our reliance on company income tax is above average (second to Norway). What do have in common with Norway? A profitable mining industry. Our company income tax is in part, a tax on mining rents (recall that the Henry Report proposed to replace part of it with a Resource Rent Tax).

Company tax revenue boomed from the early 2000s, just as the mining boom hit its straps (see the yellow line). Large reductions in iron ore and coal prices in recent years have hit company income tax revenues hard, and this is the main single cause of our present Budget problems.

Those Budgetary problems are getting worse. While we clearly can’t sit back and wait for income tax bracket creep to sole them, strengthening the income tax system has to be part of the solution.

Hidden gems in the Tax Discussion Paper: Shocking news from Treasury – personal income tax as efficient as GST!

Business, Government, and “every pet shop galah” have been saying that we should rely less on income taxes and more on the GST because this would be good for the economy. In my blog ‘Who’s the fairest and most efficient of them all?” earlier this year, I challenged this view.

Treasury modelling of the economic impact of different taxes tucked away on p32 of the Government’s Tax Discussion Paper confirms my doubts. It should change the debate.

Now, Treasury has released the details of that modelling.

Here’s the graph from the Discussion Paper comparing the “marginal excess burden” (efficiency loss) of different taxes. The marginal excess burden is the loss of future spending power across the economy per dollar of revenue raised from a tax. A low MEB means a tax is efficient; a high one suggests we might look elsewhere for public revenue.  The “efficiency ranking” of taxes here is similar to other studies, with taxes on land the clear winner and Stamp Duties receiving the wooden spoon. Company income tax is growth-reducing to the extent that capital is mobile (and the assumptions the model makes about this are critical).

The “efficiency ranking” of taxes here is similar to other studies, with taxes on land the clear winner and Stamp Duties receiving the wooden spoon. Company income tax is growth-reducing to the extent that capital is mobile (and the assumptions the model makes about this are critical).

Comparing labour income taxes and GST: economically, there’s nothing in it!

But the real story is the comparison between income taxes on labour and the GST: if the Treasury’s modelling is accurate there’s nothing in it! The MEB for a flat rate income tax on labour incomes was 21%, that for the GST 19%. Contrast this with Stamp Duties at 72%, and there’s nothing in it. A flat-rate labour income tax is about as efficient as the GST (compare the two blue dots in the graph).

“Our estimate of the marginal excess burden on individual’s labour income and GST are very similar at around 21 cents and 19 cents respectively. This aligns with the intuition that taxation of labour income and GST both effect the real purchasing power of wages, with a similar incidence on labour supply.”

and:

“Compared to taxes with a relatively significant impact on economic growth and living standards (such as company tax), individuals income tax is usually considered to have a comparatively moderate impact on the behaviour of most people, and relatively minor adverse impacts on economic growth and living standards”, p41

It turns out that consumption taxes also reduce work incentives, because they reduce the spending power of wages. Indeed, tax theory suggests that consumption taxes fall more heavily on labour (and the accumulated savings of retired people) than income taxes. So a shift from taxing income to consumption is likely to reduce work incentives overall – This is argued in my blog ‘Who’s the fairest and most efficient of them all?’

Treasury’s modelling suggests that a progressive income tax (in which tax rates rise with income, represented by a dash in the graph) is less efficient than a flat one (in which tax is levied at the same rate on everyone, represented by a dot).

But here there’s a glitch in the model. Households are represented by a single family, so the model is unable to distinguish between work incentives for men and women, two income families and single income families, or families with and without children. The model simply assumes that as income tax rates rise, they have a greater (negative) impact on workforce participation. And it does not take into account the combined impact of income tax rates and social security income tests, which mainly impact on unemployed people and women in low and middle income families.

As the Treasury knows, in the real world it is low-income women not high-income men who are most sensitive to taxes when they decide whether to increase their paid working hours:

“The groups most likely to respond to high effective tax rates include the unemployed and

lower-income earners (who often work part-time). Primary care givers, such as parents with young children, are also relatively responsive to effective tax rates but they also respond to other costs associated with working, such as child care.” p45and:

“In the absence of any changes to payments or assistance, and all else being equal, targeting tax cuts at the lower end of the income spectrum should generate a higher participation response than if the same value of tax cuts were delivered at higher incomes, “p45.

So it’s not obvious that a progressive income tax is worse for labour incentives than a flat income tax. There’s abody of research that suggests the opposite.The highest income tax rates fall on married men, and the sensitivity of the working hours of married men to an increase in tax is close to zero in research cited by Treasury.

Broadening the GST: nothing in this either

The other eye opener is the difference in the economic impact of the current GST (which taxes about half of all consumption, represented by a dot in the graph) and a broad based one (which taxes all consumption, represented by an x). Again, there’s nothing in it, a difference of just 2%!

It might be tough for retailers to distinguish between the GST treatment of a pizza and a pizza roll, but it makes little difference to growth levels in the wider economy.

Income taxes and investment: more of a story here

The Treasury modelling also challenges the view that a switch away from taxing personal income would be good for investment, arguing that investment is more sensitive to global rates of return than the impact of local taxes on investment incomes.

On the other hand, it concludes that foreign investors are very sensitive to company income tax rates. The MEB for company tax is estimated at 50%. Treasury argues that company taxes ultimately fall largely on workers as a result of lower foreign investment in Australia. There are two critical assumptions here: perfect capital mobility (without which Treasury says the MEB could fall by 20%) and that ‘economic rents’ comprise about one seventh of profits taxed in Australia (if this is doubled then the MEB also falls by about 20%).

Economic rents are above-normal profits flowing from location or firm specific inputs such as natural resources. If they are taxed properly, there are virtually no adverse economic impacts because the tax has no effect on investment decisions. So the higher the proportion of company income taxes that come from economic rents, the less likely they are to have adverse impacts on the economy.

The tax that dare not speak its name – a properly designed mineral resources tax – is a tax on economic rents. This was the main reason the Henry Report argued for a switch from taxing company income generally towards a tax on above-normal profits from mineral resources.

The ideal tax: Land

Finally, since land is immovable, a broad based tax on all private land (such as council rates) has no adverse economic impacts. Indeed, the Treasury estimates it would improve economic efficiency by 10%. This positive view of the economic effects of a broad tax on Land is uncontroversial.

Don’t always believe what you read in the papers

This is a timely warning for Government, tax lobbyists, the media, and tax reform junkies. Don’t always believe what you see and hear in the news.

It’s also a warning about tax reform modelling. It’s a very imprecise science. Many people have quoted the findings of a 2008 OECD study which found that consumption taxes were more efficient than taxes on personal income. A close reading of that report reveals the caveats:

‘Estimates of the effect on GDP per capita of changing the tax mix while keeping the overall tax-to-GDP ratio constant indicate that a shift of 1% of tax revenues from income taxes to consumption and property taxes would increase GDP per capita by between a quarter of a percentage point and one percentage point in the long run depending on the empirical specification.The magnitude of the estimated effect is larger than what would be reasonably expected. Given that there is a wide dispersion of the point estimates across specifications it is clear that the size of the effects cannot be measured precisely in a cross-country comparative setting. …Thus, the magnitude of the effects should be interpreted with caution.’ (p43)

In contrast to the latest Treasury research, modelling by KPMG Econtech of the impact of different taxes on the Australian economy which was conducted for the Henry Review found that consumption taxes were significantly more efficient than personal income taxes (though the overall efficiency rankings of different taxes were the same as above).

This raises a serious question for policy makers: is our economic modelling of the impact of taxes reliable enough to draw firm conclusions for policy? This question was posed recently by a study commissioned by the Mirrlees review in the UK. The authors concluded that arguments for the removal of taxes on investment incomes were getting well ahead of the reliability of the research.

If the impact of greater reliance on consumption taxes on the economy is uncertain, its (regressive) impact on household spending power is clear. (see my blogs: ‘Who’s the fairest and most efficient of them all?’ and ‘ACOSS report shows taxes are lower and less progressive than people think.’)

It’s time to move on from the unproductive and divisive debate over whether to tax consumption more and income less, and get down to the business of making both income and consumption taxes fairer and more efficient. There’s plenty that needs to be done.

Is there a magic pudding?

A quick analysis of CPA Australia’s GST proposals

This is a quick off the cuff analysis of CPA Australia’s report: Tax reform in Australia, the facts, a day after its release. In the absence of time to study the report more closely, and critical details of the modelling and presentation of data, I raise as many questions as answers. But they are important questions – including how a revenue neutral change in the tax system leaves all households better off. There are efficiency gains from good tax reform but the magic pudding remains elusive!

The CPA proposals are a welcome change from standard ‘tax mix shift’ reform proposals which trade off a higher GST for lower income taxes. Instead, most of the revenue gained from higher GST would be used to remove some of the most inefficient (and unfair) State taxes such as Stamp Duties on insurance. Aside from the proposed income tax cuts, most of the taxes to be replaced fall mainly on household consumption, so the implications for the distribution of spending power among households are less clear cut than a straight consumption tax for income tax switch, which is strongly regressive. See my previous blog ‘Who’s the fairest of them all’ and ACOSS analysis ‘Paying our fair share’.

The CPA advances four reform options:

- A 10% GST with health, education and fresh food exemptions removed to raise $12B in 2015 to replace stamp duties on insurance & motor vehicles ($8B) and modestly reduce property Stamp duties and other indirect taxes ($2B), with the remaining $2B used for income tax cuts and an increase in income support payments.

- A 15% GST off the existing base to raise $26B to replace stamp duties on insurance & motor vehicles ($8B), substantially reduce property Stamp Duties ($10B) and other indirect taxes ($2B), with the remaining $6B used for income tax cuts and an increase in income support

- A 15% GST with health and education in the base to raise $37B to replace stamp duties on insurance & motor vehicles ($8B), abolish property Stamp Duties ($13B) and other indirect taxes ($2B), with the remaining $14B used for income tax cuts and an increase in income support

- 15% GST with health education and fresh food in the existing base to raise $42B to replace stamp duties on insurance & motor vehicles ($8B), abolish property Stamp Duties ($13B) and other indirect taxes ($2B), with the remaining $19B used for income tax cuts and an increase in income support.

Using a model developed by KPMG, the report estimates the impact of these options on economic growth and on households (divided into groups of 20% by household ‘equivalent’ income). It also makes a number of claims about the inefficiency of the current tax ‘mix’. This blog is in two parts: ‘what’s clear’ (some obvious points) and ‘what’s not clear’ (questions that need to be clarified).

What’s clear

1. Australia does not rely a lot more on income taxes (broadly defined) and a lot less on consumption taxes, than the OECD average.

The international tax revenue data in the report shows that, when social insurance contributions in other OECD countries are added in, 58% of tax revenue in Australia comes from taxes on income compared with an OECD average of 60% – or 63% compared with 61% if Payroll taxes are included (figure 2-8)

The share of tax revenue raised from consumption taxes is 27% in Australia compared with an OECD average of 33%. There’s much more to consumption taxes than GSTs and VATs, including State taxes such as Stamp Duties that fall on consumption.

2. The increases in the GST modelled for the report by KPMG would reduce economic growth for the first three years after the reform.

It is well known that one of the short term effects of an overall rise in consumption taxes is that the economy slows, due to the impact of higher prices (just ask the Japanese). To be precise, it increases household consumption in the years between announcement of the reform and implementation as people rush to buy good at existing prices, then reduces it).

3. Abolishing inefficient State taxes would boost growth in the long run

It’s not surprising the modelling finds that GDP would grow faster over the long term if these taxes were abolished. Taxes such as Stamp Duties have well known negative impacts on investment and growth. Taxing business ‘inputs’ rather than final income or consumption or assets such as land and mineral wealth is inefficient as it distorts household and business investment decisions (for example by discouraging people who need it from taking out insurance, and penalising decisions to move house).

The $27.5 billion dollar question is: by how much? This is notoriously difficult to estimate. As with all macro-economic modelling, results depend on assumptions. The report appears to take this a step further by assigning the projected economic efficiency gains to households (which no Government would be brave or foolish enough to do).

4. Low income households don’t usually benefit from tax cuts

One quarter of households, including the vast majority of those in the bottom 20%, pay no income tax (but they do pay consumption taxes), so they would be worse of in the absence of social security payment increases if consumption taxes increased.

As the above ACOSS report argues, relying on social security payment increases to sustain spending power is risky in an environment when these payments are under threat (see last year’s Budget)

What’s not clear

1. Why do all households gain from revenue-neutral tax reforms?

All four proposals are revenue neutral. They neither increase nor reduce taxes overall. So in the short term, reform is a zero sum game with winners and losers. Yet all households appear to win in the modelling.

A close look at Appendix ‘C’ shows that his happens because of a line item called ‘increase in income before tax’. Why would income increase before tax (apart from social security payments increases which are accounted for separately)?

One possible reason is the claimed ‘efficiency dividend’ from the reform. That is, the economy grows more quickly because taxes are less distortionary. But that’s a long term impact. As indicated, the model shows that GDP growth slows for the first three years and household consumption is projected to fall for the first five years.

If ‘input taxes’ (such as Stamp Duties) are replaced by a tax on consumption (like the GST) we would expect households to be slightly worse off in the short term, in the absence of compensation. This is because in the short term, some of the gains from abolition of input taxes would ‘leak’ to sectors other than Australian households (especially exports).

2. What happens of we exclude ‘increases in income before tax’ and focus on the impact of the tax changes?

If we separate out the effects of tax and social security changes (higher GST, lower Stamp Duties, and income tax cuts and social security increases) from the projected ‘increases in income before tax’ we find that the first reform option (removal of GST exemptions, abolition of some Stamp Duties, a reduction in the first marginal tax rate from 19% to 18.5%, and modest social security increases) reduces household spending power for the bottom 2 quintiles and raises it for others.

This is the pattern of short-term winners and losers we would expect from such a change (red bars), though the average losses at the bottom end are much larger than expected:

- Low income households are disproportionately affected by the consumption tax changes

- Since only the lowest marginal income tax rate is cut, middle income households gain the most, but high income earners also gain because the tax cuts flow through to them as well.

When the ‘increases in income before tax’ are added in (blue bars) everyone wins and the reform is distributionally neutral (see Figure 3-4 in the report).

But where do these income increases come from? The report refers to ‘increased incomes as a result of improved efficiency in the economy’ (p14). If this is where they come from (and these look like brave assumptions), how would these efficiency gains flow through to households in the first year of the reform (2015-16)?

3. What is the effect of the consumption tax changes on their own?

It would be worth knowing what the effect of replacing Stamp Duties with a higher GST has on the spending power of households at different income levels, since this kind of reform is rarely modelled. The impacts are not obvious since Stamp Duties themselves largely fall on household consumption – so the reform would replace one set of regressive taxes with another. Its effects would depend on the spending patterns of different households (e.g. on food, home purchases, car purchases, insurance, etc).

It’s good to see more information out there on the impact of different tax reforms, and it would be even better if some of the results in the report were explained more fully.

The ‘size of Government’ obsession

This week, the PM suggested we do what the New Zealanders had done and put a cap on the size of the Federal Government.

‘And one of the points that I made in my speech to the Press Club last week is that if you look at what New Zealand did with fiscal consolidation, they had a very tight clamp on new spending. They didn’t engage in big cuts. They had a tight clamp on new spending and New Zealand has got government, as a percentage of GDP, from 35 per cent to 30 per cent – a very big change in just a few years.’

The suggestion is that rather than change the direction of policy (by raising taxes or cutting spending more fairly), the Budget will just move more slowly in the same direction, or perhaps not at all! With no steering, no acceleration and no brake, there’s not a lot of room for the next Budget to move. Might as well garage it for a year and avoid the political angst!

Let’s set aside the important question of whether the Budget should stimulate the economy or consolidate public finances (last year’s Budget struck a sensible balance on that score – the big cuts were postponed to future years, but the recent RBA decision to cut interest rates shows that circumstances have since changed for the worse).

The-not-so hidden assumption behind the PM’s statement, and last year’s Budget, is that smaller Government is better. That’s why all of the action in last year’s Budget was on the spending side. Given the targeting of most public spending in Australia, that almost inevitably means the Budget was a regressive.There’s not much room for large cuts outside social security, health and education.

Yet, as ACOSS argued in its Commission of Audit submission in 2013, most of the damage to the Budget bottom in recent years came from sliding revenues, not higher expenditures.

There’s on old neo-liberal economics argument that smaller Government is better for long term economic growth (setting aside any temporary economic stimulus) because taxes and spending dampen and distort market signals in the economy.

In the same submission, ACOSS addressed this issue by dipping into what economic research said about the size of Government and economic growth. It turns out that that there is a (loose) association between size of Government and economic growth, though it is hard to clearly identify the impact of public spending and taxing given all of the other factors that determine long term growth levels. There’s also the problem of reverse causation: the slower the economy grows, the higher is public spending on unemployment and other benefits.

But the real story is not about the quantity of public spending and taxing, it’s the quality that matters for long term growth. Some forms of spending, such as public infrastructure investment, are more growth enhancing than others. Countries that achieve their social goals in a cost effective way are also more likely to be rewarded with stronger economic growth.

The size of Government is mainly a political (and ideological) decision, not an economic one.

Here’s an extract:

ACOSS Commission of Audit submission (2013)

Appendix 5: The ‘size of Government’ and economic growth.

The effect of the size of public revenues and expenditures on long term productivity and economic growth has been vigorously debated for many years. In studies exploring this relationship, ‘size of Government’ is usually proxied by public revenues (or tax revenues) or public expenditures as a proportion of GDP. Early studies suggested that there was an optimal size for Government, above which future economic growth would be constrained.43 A number of subsequent empirical studies of the public revenues and expenditures and economic growth have found that higher revenues and expenditures are associated with slower long-term growth in wealthy countries.44

However, it does not follow from a simple association between Government size and economic growth that one ‘causes’ the other. There are four problems with this apparently ‘simple’ story:

1. The character of public spending and taxes may be as important as its ‘size’. Studies have found that pubic investment in physical infrastructure and human capital development (education) are positively associated with economic growth. Much of what is usually classified as ‘social expenditure’ promotes employment participation and productivity. More broadly, the efficiency of the public sector matters.45

2. Whether or not the size of Government has an impact on economic growth, other policies may have a countervailing effect. While long term economic growth rates have been stronger in recent decades in the Anglo-Saxon countries (which have below average tax levels) than in continental Europe (with above average tax levels), the Nordic countries have both high tax levels and high long term economic growth rates (see table below). One suggested explanation is that the economic openness of the Nordic countries more than compensates for their relatively high tax and expenditure levels 46 .

Tax levels and growth in three types of welfare systems

| Country group | tax to GDP ratio (%) | Average annual real GDP growth (1995 to 2004 – %) |

| Nordic | 45.7% | 2.5% |

| Anglo-saxon | 31.6% | 2.3% |

| Continental European | 38.8% | 1.5% |

Bergh & Henriksen, 2011, ‘Government Size and Growth: A Survey and Interpretation of the Evidence’, Research Institute of Industrial Economics, IFN Working Paper No. 858, 2011 Stockholm.

3. Causation may be in the opposite direction. For example, slower long term growth rates in many continental European countries may be associated with higher unemployment rates (which increase the cost of unemployment benefits) or older populations (which increase the cost of pensions and health care services).

4. In any event, Australia, which is the third-lowest spending country in the OECD, and has a relatively cost efficient social security system and human services, has considerable room to move before higher public revenues and expenditures put a brake on economic growth.

43. For example, Barro 1990, ‘Government spending in simple model of endogenous growth’, Journal of Political Economy Vol 98, No5.

44. Bassanini and Scarpetta 2001, ‘The driving forces of economic growth’, OECD Economic Studies No 33.

45. Angelopoulos et al 2008, Does public sector efficiency matter? Revisiting the relation between fiscal size and economic growth in the world sample, Public Choice, Springer, vol. 137(1), pages 245-278

46. Bergh & Henriksen, 2011, ‘Government Size and Growth: A Survey and Interpretation of the Evidence’, Research Institute of Industrial Economics, IFN Working Paper No. 858, 2011 Stockholm

A brief history of tax (Part 1) Income tax, the great leveller.’

‘The tax code, once you get to know it, embodies all of the essence of life: greed, politics, power, goodness, charity. Everything’s in there.’ Sheldon Cohen, Former Commissioner of the IRS.

Tax reform is back on the agenda. Since those who fail to study history risk repeating it (and I was involved in the latter-day history of tax reform) I’m writing this 3 part series as a guide for people who want to become involved in the next phase. I begin with a short history of the dominant tax of the second half the 20th century – personal income tax.

To keep it simple, I’ll focus on some of the big debates over the goals of tax reform and how the system should be restructured to achieve them. Readers with an interest in detail can buy a book, such as Julie Smith’s excellent ‘Taxing Popularity’ (a history of Australian tax policy to 2004) or Slemrod & Bakija’s ‘Taxing ourselves’ (MIT Press 2008 – a beginners guide to tax policy from the US); or turn to the ‘Henry’ Report’s Architecture of the Australian Taxation System . Those wanting to keep up with current Australian tax debates should visit the Tax Watch site.

For most of the second half of the 20th century, the income tax was king. It raised over half of all public revenue in Australia. In the eyes of its supporters it was a benevolent king because it taxed fairly.

What’s income?

Income is a surprisingly slippery concept. The first step in taxing it was to define it. One of the earliest definitions came from Robert Haig:

‘ the money value of one’s net accretion to one’s economic position between two points in time.’ Haig, R (1921) The Federal income tax, New York: Columbia University Press, p27.

In plain language, income is ‘spending power’. A decade and a half later Simons refined Haig’s definition – as the sum of (1) consumption of goods and services in the market and (2) the change in the value of personal wealth in any period. The second part of this equation is the basic difference between a tax on income and a tax on consumption – unlike a consumption tax, an income tax captures the annual returns from that part of income which is saved and invested.

Most people associate income taxes with deductions from their fortnightly pay, yet income has many other guises: interest, dividends, capital gains (the annual change in the value of an investment asset such as shares or property), and ‘imputed rent’ from housing (the annual rental value of the housing ‘services’ you receive when you own your home). A ‘comprehensive income tax’ taxes all of these items at the same rates. All of these items reflect changes in an individual’s ‘spending power’. Note that an income tax is also different from a wealth tax (including taxes on land), which taxes the stock of an individual’s wealth rather than annual changes in its market value.

To illustrate the difference between spending and spending power, let’s compare two people who each spent $50,000 last year. One had an income of $50,000 and spent all of it on regular living costs (as around half of all Australian households do). The other had income of $70,000 and saved $20,000 for a home deposit. She was in a stronger economic position because she had an extra $20,000 and could choose to spend it now or save to improve her future spending power. The difference between income and spending is, of course, saving. It’s all a matter of timing – people either spend their income now or save in order to defer their spending.

Why tax income?

For Haig, the purpose of income tax was to tax people more precisely according to their ability to pay, and their spending power was the best way to measure this. (this is hotly debated by advocates of a shift towards consumption taxes, on which see Part 2). This was the ‘soft’ version of the purpose of income tax. The ‘hard’ version was enunciated by Henry Simons at the tail end of the Great Depression. He argued that its purpose was for:

‘altering or correcting the distribution of wealth and income’. Simons H (1938), ‘Personal income taxation: ‘The definition of Income as

a problem of fiscal policy,’ Chicago: University of Chicago Press, p15.

Despite the sharp political divisions at this time – US President Roosevelt announced at a public rally that he ‘ate capitalists for breakfast’ – the hard version was not the main motive for the dramatic increases in income tax over the next decade. Income taxes were used to fund two world wars.

Income tax and war

As in the US, the first national income tax was introduced in Australia to finance the war effort (the First World War, that is, in 1915). At the time most public revenue came from customs and excise duties – taxes on consumption. These fell on unemployed people and pensioners as well as wage earners, and low paid workers as well as high income earners. Economic divisions were much sharper than than now: unemployment was high and most wages were close to subsistence levels. The vast bulk of private investment income went to a wealthy minority. The new income tax was not consciously used by the Hughes Government to redistribute income, but in financing the war it could not ignore the economic inequalities and social tensions of that era. It was time to shift some of the tax burden to those with higher wages and income from investment.

The first national income tax included investment income, it had steeply progressive marginal tax rates and it wasn’t levied at all on the majority of wage earners. It was accompanied by federal taxes on undistributed company profits, land and inheritances. A country which previously had one of the most regressive tax systems in the western world (that is, one in which effective tax rates are higher for low income earners than for high income earners, in proportion to their incomes) now pioneered an income tax with multiple rates. But to put this in context, Federal and State income taxes together raised less than 10% of all public revenue.

The next step was a dramatic rise in federal income tax revenues in the early 1940s to fund the second (world) war effort and the extension of social security entitlements to unemployed people. There was also a push to centralise income tax in the hands of the Commonwealth to facilitate economic management (State income taxes preceded the national one). Low paid workers were income-taxed for the first time but ‘unearned’ income from property was taxed at higher rates than wages. By the late 1940, income tax raised more than half of all public revenue.

The income tax scale was steeply progressive: for much of the post-war period, the top personal tax rate was over 60% and the company tax rate was over 40%.

Income tax as a leveller

There can be little doubt that the personal income tax redistributed income on a large scale, whether that was its purpose or not. One of Picketty’s main conclusions in his magnum opus Capital in the 21st Century was that the expansion of income taxation in wealthy nations from WW1 on was a major cause of the decline in income inequality over the next 50 years.

This graph shows the typical pattern of income inequality in wealthy countries over the second half of the 20th century, in this case among Australian males (old data are all too often male!), from Andrew Leigh’s research. Inequality moved over this period in a ‘U’ shape curve, higher in the ’40s, falling to a low point around the late ’70s, then rising steadily. [The higher the ‘gini coefficient’, the more unequally distributed income is – if the gini has a value of 0 all income is shared equally, if it has a value of 1 all income is held by one person.]

You can also see from this graph that the income tax system (the only taxes in Leigh’s data) reduced inequality among Australian men by about one quarter between the ’40s and the ’90s. If the same data were available for the first half of the century, they would show a much smaller impact since the income taxes themselves were much smaller. Inequality of private incomes was also greater at the turn of the 20th century.

Another way in which high top tax rates might reduce inequality is through behavioural effects. Picketty argues that confiscatory tax rates on very high incomes after WW2 discouraged employers from paying high wages in the first place, and indeed growth in top wages moderated during and after the war.

Causation also worked in the opposite direction: growth in income taxation was part of a wider push to temper the harsh inequalities and suffering of the great depression and to ‘win the peace’. The rise in Australian income tax in 1944 was to pay for social security for unemployed people and widows. Full employment was enshrined at the centre of economic policy. Minimum wages rose and unions grew stronger. All of these factors contributed to the reduction in inequality from the 1940s to the 1970s. Then public policies began to swing in the opposite direction.

War on income tax

The equalising effect of personal income tax declined from the 1980s as the tax rate scale became less progressive (redistributive), and then as the overall size of the personal income tax was reduced through eight annual tax cuts during the 2000s. This has been the trend across many OECD countries (see below).

In the 1970s and ’80s, the income tax system fell out of favour with policy makers and sections of the public. This was part of wider shift in the policy zeitgeist from reducing inequality to removing constraints on economic growth. It was also due to serious flaws in the income tax system itself which were exposed at a time when inflation averaged over 10% per year. People were moving rapidly into higher tax brackets, and those in the top brackets were making greater efforts to avoid tax. One prominent national daily newspaper declared a ‘tax revolt’. The king seemed to have lost his clothes!

‘Increased revenue demands are being placed on a system that contains some basic structural flaws and a tax base that has been whittled away through special concessions and tax minimisation arrangements. The system has been criticised by officially commissioned inquiries, (including the Asprey, Mathews, and Campbell Committees), academics, the media and, increasingly, the general public. The system’s basic unfairness, its complexity, and its adverse effects on incentives to work, save, invest and take risks are widely recognised. In short, respect for the system, which is essential for voluntary compliance, has been seriously undermined.’ (Australian Government (1985), Draft White Paper: Reform of the Australian Taxation System, p18)

In the 1970s the Asprey Report diagnosed the problem as an engineering fault: tall tax rates were built on a narrow foundation and the building was at risk of collapse. It advocated a trade-off between a ‘broader tax base’ (the removal of shelters and loopholes) and lower rates. Crucially, this was argued on economic efficiency as much as equity grounds. The tax system was distorting investment decisions (for example the lack of a tax on capital gains encouraged speculation in asset values, especially housing) and labour force participation (due to high marginal tax rates).

Mathews argued that inflation was white-anting the tax system and the best way to bring it back into equilibrium was to adjust income tax thresholds and investment returns for inflation. The latter idea was consistent with the original theory of taxation of investment income, that only ‘real’ (after-inflation) returns should be taxed. Asprey and Mathews didn’t want to bury the income tax, they wanted to save it. Mathews famously argued that the challenge was:

‘not to make the rich pay higher rates of tax, or even more tax, than the poor; it is to make the rich pay any income tax at all.’ Mathews R (1981), ‘The structure of taxation’.

These reports gathered dust until a Royal Commission was established into a very different matter: the activities of the Ship Painters and Docker’s Union. The Fraser Government forgot the first principle of public inquiries – don’t set one up unless you already know the outcome! What started as an inquiry into the nefarious activities of a trade union became a public airing of tax evasion at the top end of town. Investment income and profits were stripped from companies before tax was payable and company records were sent to ‘the bottom of the harbour’. This was the last straw for many ordinary wage earners, whose tax rates rose all too frequently as inflation pushed them into higher tax brackets.

RATS save the ship

The income tax was finally patched up in 1985 following the Hawke Government’s Tax Summit. This was a time when different sectors of the community – unions represented by the ACTU, the community sector by ACOSS, and major business organisations – were encouraged by Government to come together to tackle the big problems of the day. It was no coincidence that this was also a period of sweeping economic and social reform.

The Treasury released a Draft White Paper called ‘Reform of the Australian Tax System’ (RATS). Thus began the tradition of applying animal names to tax reforms. This one may have been borne of frustration – Treasurer Keating’s preferred ‘Option C’ which included a ‘broad based consumption tax’ (another recommendation of the Asprey report) was dropped (more on this in Part 2).

The RATS package attempted to seal the four main ‘cracks’ in the income tax system (see Rick Krever’s summary of the package and its origins).

First, the different tax treatment of capital gains (which were largely untaxed) and other investment income: A Capital Gains Tax was introduced on increases in the value of assets such as shares and property (but not the main residence), after taking account of the effects of inflation (but inflation adjustment was not extended to other investments as Mathews proposed so investments were still taxed inconsistently).

The second problem was related to the first: the mismatch between income and deductions in ‘negatively geared’ property investments. Real estate investors structured their affairs so that annual investment expenses (e.g. interest payments on debt) exceeded returns (e.g. rents) for a number of years before the property was sold, yielding a low-taxed capital gain. The problem for the fisc was that these ‘losses’ were deducted against other income (e.g. wages) which were taxed every year at higher rates than capital gains. There was a mismatch between the timing and the level of income tax and related deductions.

Third, a Fringe Benefits Tax was introduced to capture income in the form of goods and services provided in lieu of wages, such as company cars (but not discounted shares and options).

Fourth, inconsistencies in tax rates applying to individuals who used different business and investment structures were tackled. It was argued that as long as the company income tax rate was less than the top personal tax rate, high income-earners could shelter their income in a private company. This problem was resolved a few years later when the company tax rate was increased to the same as the (lowered) top personal tax rate, but this alignment of the two tax rates only lasted a few years.

The tax bias in favour of diverting income into private discretionary trusts also attracted attention. This problem would be partly resolved by reducing the value of the tax breaks (such as building depreciation) that flowed through to the beneficiaries of these trusts. This reform, which brought their tax treatment more closely into line with that of companies and fixed trusts, was later reversed on a legal technicality and the use of private discretionary trusts to avoid tax continued apace.

The RATS reforms were vigorously opposed amid warnings that the sky would fall in on business lunches, the car industry and rental property investment. While it’s true that the ‘abolition of negative gearing’ for rental property introduced a tax bias against borrowing for housing investment relative to other investments (e.g. borrowing to buy shares), the claim that it decimated rental property investment was false – investment only declined in Sydney and Perth and the main reasons for this were interest rate increases and a sharemarket boom (see Badcock & Browett (1996), ‘The responsiveness of the private rental sector in Australia to changes in Commonwealth taxation policy’). Despite this, this federal tax reform was reversed during a hard fought NSW election campaign, to avert a scare campaign over rent increases.

As it turned out, the sky remained in its place, the restaurant industry prospered and the car industry continued to post losses as it had for some time. The reforms were widely accepted because the the majority of taxpayers received tax cuts at the expense of the minority who previously benefited from tax shelters. The top tax rate fell from 60% to 49% but more high income-earners would at least pay the 49%. In one swoop, RATS attacked the two main public complaints about the income tax.

A startling fact about the RATS reforms was that their logic – to ‘broaden’ the tax base and lower rates – was identical to a simultaneous tax reform in the US authored by the Reagan administration. Like Keating, Reagan was determined to cut income tax rates, including the top rate. His problem was that after he cut tax rates dramatically in 1981 the US budget fell into deficit (contrary to the theory that lower tax rates might increase revenues, promoted by economist Arthur Laffer). If he was to cut income tax further he would have to find a way to pay for it. The solution proffered by the US Treasury was the same as its Australian counterpart: close or restrict tax shelters. The US Capital Gains Tax was increased, negative gearing was restricted, and depreciation allowances for business were cut. Reagan’s political strategy was the same as Keating’s – those who opposed the removal of tax shelters would be accused of standing in the way of tax cuts for the majority. The story of this hard-fought battle for tax reform in the US is detailed in Birnbaum & Murray’s entertaining and informative ‘Showdown at Gucci Gulch’ [Gucci Gulch was the area outside a certain Senate Committee room where tax lobbyists gathered].

The king faces a challenger

While many gaps remained in the income tax – including those that were re-opened following the retreats on negative gearing and discretionary trusts – it remained the pre-eminent Australian tax. Yet by the end of the 1980s the income tax still faced challenges on two fronts. It was under siege politically due to its high visibility and the general retreat from inequality-reducing policies. It was also threatened intellectually by a new challenger, the broad based consumption tax. The battle of ideas often precedes the political one, and so it was with tax policy. The idea that the income tax should be replaced by a tax on expenditure was first advanced in the 1940s. This is the topic of Part 2 of the Brief History of Tax, the Clash of the Titans.

Brief History of Tax, Part 2: Clash of the Titans

‘The tax code, once you get to know it, embodies all of the essence of life: greed, politics, power, goodness, charity. Everything’s in there.’ Sheldon Cohen, Former Commissioner of the US Internal Revenue Service.

A brief history of tax (Part 2): Clash of the titans

Tax reform is back on the agenda. Since those who fail to study history risk repeating it (and I was involved in the latter-day history of tax reform) I’m writing this 3 part series as a guide for those involved in the next phase. Part 1 dealt with the dominant tax of the second half the 20th century – personal income tax. This part describes the intellectual and political contest between taxing income and consumption over the last four decades: a clash of tax titans.

Readers with an interest in detail can check out the references in Part 1 of this blog. In addition, good summaries of the arguments for and against a switch from taxing income to taxing consumption are provided by Brooks, Auerbach, and Henry. Those wanting to keep up with current Australian tax debates should visit the Tax Watch site.

Re-capping the income tax story

By the 1970s the income tax was ‘king’. Personal and company income taxes raised the majority of public revenue in Australia. Income tax was a key tool for redistributing resources from those with the greatest ability to pay – those with higher incomes – towards those with the least. Elite and public support for income tax faded during the 70s and 80s for a complex set of reasons: inflation was moving ordinary wage earners into higher tax brackets while high income earners could readily avoid paying tax. At the elite level, redistribution was out of favour as wealthy nations grappled with the failure of the post-war economic model to deliver steady growth in living standards. The neoliberal view – that these problems could only be resolved if constraints on the free operation of markets were removed – gained traction.

One of the constraints identified at this time was the income tax system, which distorted saving and investment decisions (these were too often made for tax reasons rather than to achieve the best returns) and discouraged workforce participation. These economic efficiency concerns carried more weight in tough economic times.

They did not necessarily conflict with equity concerns. Neoliberal economists were among the strongest supporters of a comprehensive income tax – one which taxed all forms of earned income and investments consistently. That meant the removal of tax shelters and loopholes which mainly benefited people with high incomes. The major Australian tax reviews in this period advocated the perfection of the income tax model, not its abandonment.

Yet there was an alternative to reconstructing the income tax. The Hawke Government’s 1984 ‘Draft White Paper’ on Tax Reform advanced three options: Option A cut income tax rates by closing tax shelters, Option B added to this reform the replacement of a ramshackle set of federal sales taxes with a broad based tax on consumption. Option C went a step further by increasing the proposed consumption tax to pay for deeper income tax cuts. Option B was an internal clean-up of consumption taxes. Option C had the more ambitious aim of changing the mix of taxation from income to consumption, or expenditure.

While it only came into prominence in Australian public debate in the 1980s, the idea that a broad based tax on consumption was superior to an income tax had deep historical roots. At its core, this was an argument about the tax treatment of saving and investment.

The expenditure tax alternative

‘The Equality of Imposition consisteth rather in the Equality of that which is consumed, than of the riches of the persons that consume the same. For what reason is there, that he which laboureth much, and sparing the fruits of his labour, consumeth little, should be more charged, than he that living idlely getteth little, and spendeth all he gets: seeing the one hath no more protection from the Commonwealth than the other? But when the Impositions are layd upon those things which men consume, every man payeth Equally for what he useth: Nor is the Common-wealth defrauded by the luxurious waste of private men.’ Hobbes Leviathan Ch. XXX. (from Kaldor, see below)

Hobbes’ 17th century ‘moral’ argument for taxing expenditure instead of income seems curious today since the purpose of saving is to make room for more spending later on. If we all ‘consumed little’ the economy would grind to a halt.

The modern-day case for taxing expenditure instead of income was first advanced by an American economist, Irving Fisher in 1942. This argument would rage among tax experts, out of earshot of the general public, for the next half century and beyond.

Fisher’s case for a tax on expenditure seems far removed from Australian public debate over sales taxes like the GST. Yet it is about the same issue: how savings should be taxed.

Just as the top income tax rate in the US reached its zenith (a top marginal rate of 80%) during World War 2, Fisher proposed an alternative, the spendings tax. Fisher’s main objection to the income tax was that it unfairly penalised saving since (as I pointed out in Part 1) it taxed investment income as well as wages and this amounted to ‘double taxation’ of savings. His solution was to remove the taxation of investment income by taxing cash-flows instead of income.

To simplify, the tax base would be the difference between cash on hand at the beginning of the year together with wages and cash income from investments accrued during the year, and cash remaining at the end of the year. The difference was the amount spent during the year. His proposed ‘spendings tax’ was actually a tax on consumption (income minus saving), but unlike sales taxes it would be raised directly from the taxpayer rather than indirectly from retailers (who then pass it on to the consumer).

The above quote from Hobbes was the opening page of Nicholas Kaldor’s book ‘An expenditure Tax’, published in 1955. Kaldor brought the idea of replacing the income tax with a tax on expenditure to the United Kingdom. This idea gained greater prominence after the release in 1978 of a landmark report by the Institute for Fiscal Studies, the ‘Structure and reform of direct taxation’. The report, prepared by an expert committee headed by James Meade, argued for replacement of the income tax with a ‘progressive expenditure tax’:

‘A progressive expenditure tax is the one form of tax which could have the political appeal of encouraging enterprise and economic development and at the same time heavily taxing high levels of consumption expenditure which at present, if it is financed out of capital, goes untaxed.’ p33

Equity and efficiency arguments

These were bold claims, and they conflicted with the common sense view that taxes on consumption were regressive. Meade and other expenditure tax advocates were not arguing the community should accept a less equitable tax system in order to promote economic growth. They were saying we could have our proverbial cake and eat it, too.

The equity case for progressive income taxes rests on two main arguments: that they tax individuals directly at progressive marginal rates and that income is a better measure of the resources available to people than consumption.

By contrast, existing consumption taxes were imposed ‘indirectly’ as sales taxes on retailers and not ‘directly’ on consumers. This meant that they ignored differences the overall level of consumption among people of different means. It was not possible to tax consumption at progressive rates using a sales tax (this could only be done imprecisely by taxing luxuries at higher rates).

Fisher, Kaldor, and Meade’s solution to this problem was a ‘direct expenditure tax’. Instead of taxing consumers indirectly via retailers, they would be taxed directly on their consumption. This could be done by converting the income tax into a tax on spending. The key was to remove from taxation that part of income which is saved. Meade described a number of ways in which this could be achieved. One option was to deduct from tax any amounts saved during the year (e.g. outlays on new investments or repayment of loans). Another option was to exempt investment income (such as interest and dividends) from tax. These changes would be coupled with the taxation of any reduction in savings as they were drawn down to be spent (as superannuation benefit payments were previously taxed in Australia). Since each individual would be taxed directly on their income minus amounts saved, tax could still be levied at progressive rates.

This focussed debate on the real difference between taxing income and consumption – the tax treatment of savings. The equity case for income taxes rests on the idea that income or ‘spending power’ is a better measure of ‘ability to pay’ than expenditure because the ability to save and invest part of our income enlarges life choices (for example, to improve housing security by buying a home). Consumption tax advocates put the contrary view: that spending is a better measure of access to resources and that by taxing the returns from saving, an income tax favours current spending and penalises future spending.

A related argument is whether ‘ability to pay’ is best measured each year, or across the life course. An annual measure favours income taxes (since income taxes impact less on people whose ability to save is constrained), whereas consumption tax advocates argue that their tax is fairer on a lifelong basis (since income must eventually be spent and it is best not to interfere with people’s choices to save and defer their spending). Of course, not all income is spent during our lifetimes: many people leave part of their wealth to the next generation. To deal with the equity objection that taxation of savings could thus be deferred indefinitely, consistent expenditure tax advocates (including Meade) argue for taxes on gifts and inheritances.

A key question from an equity point of view is whether people who are relatively well off derive more benefit from a tax system that allows them to defer taxation on income from their savings until they spend it.

Key issues from an economic efficiency point of view are which of these two tax bases have the least adverse impact on saving, investment, and workforce participation, with a minimum of distortion of decision-making in each of these areas.

I’ll deal with these issues in a separate blog: ‘Who’s the fairest (and most efficient) of them all?’ For now, let’s turn to how the clash of these two tax titans – income and consumption taxes – was resolved in Australia and other wealthy countries.

The tax mix hasn’t changed much at all

If we take a virtual trip to Cabarita Beach in northern NSW, we’ll find this sign:

‘Historic site: At this precise point, on the morning of December 12 1927, nothing of significance is known to have occurred.‘

The outcome of the argument over the optimal tax mix feels a bit like this.

On the face of it, 40 years of fierce intellectual and political argument over the ideal tax mix has had little impact on the balance between income and consumption taxes in wealthy countries. What it has achieved is a more nuanced view of the taxation of income and savings, informed by a substantial body of research.

The share of consumption taxes in public revenue of OECD countries (top line) fell during the 1970s and has been stable since. This is the result of two conflicting trends: a decline in customs duties and taxes on specific goods offset by a rise of broadly based ‘value added taxes’ such as Australia’s GST.

The revenue share of income taxes also remained stable, but this masked major changes in the composition of taxes on income.

The key change here over the last 40 years was a reduction in the share of personal income taxes (top line), offset by a rise in social security taxes (second line). These taxes, used in Europe and the US to finance social insurance payments, are usually raised at a flat rate.

This change, along with less progressive income tax rate scales, reduced the progressivity of income taxes. Interestingly (given arguments that company income taxes would be competed away), the share of corporate tax revenues (bottom line) remained stable, even rising in the 1990s.

Enduring differences in the tax mix among countries

There are enduring differences in the tax mix and revenue ‘take’ between the Anglophone countries and most of Europe. The Anglophone countries raise less tax overall but do so more progressively, with a greater reliance on progressive income taxes. Most European countries raise more revenue, but rely less on income taxes and more on consumption or social insurance taxes to do so.

As shown in an OECD analysis, these international differences reflect different strategies to redistribute income in European and Anglophone countries. Across northern and central Europe, generous social insurance payments for retirees, people with disabilities and unemployed people play a major role. These require much higher taxes, and European countries are more tolerant of less progressive tax systems as long as they raise the revenue needed for these and other social programs. Australia, the US and Canada have more parsimonious social security systems and their electorates are more sensitive to any reduction in the progressivity of the tax system. This reflects the Anglophone emphasis on ‘targeting’ of both benefits and taxes to achieve distributional gaols with smaller welfare systems.

An exception is New Zealand, where social security payments are low and Governments have reduced the progressivity of the tax system by cutting top marginal tax rates and increasing the GST. New Zealand Treasury analysis found that recent changes along these lines in 2010 had little impact on the real disposable incomes of households on less than $NZ20,000 but boosted those of households earning over $NZ200,000 by an average of almost 3%. Tax policy changes along these lines, together with radical deregulation of the labour market, have led to one of the largest increases in income inequality among OECD countries over the last 30 years, with the gini coefficient rising from 0.27 (well below the OECD average) to 0.33 (slightly above it).

What happened in other countries?

In Europe, the major change to consumption taxes since the 1970s was the increased use of broad-based Value Added Taxes (like our GST, these tax the increase in the value of a product at each stage of its production and sale, offset by refunds for the cost of inputs). But the replacement of narrowly based consumption taxes and customs duties with VATs was part of a European Union push to modernise and standardise consumption taxes. It was not an attempt to replace income taxes.

The introduction of VAT by the Thatcher Government in the UK followed this logic. The Meade Report was not well received by her Ministers, who were wary of his proposed gift and inheritance tax and believed an incremental approach to tax reform was more likely to succeed than replacing the income tax with a new tax on expenditure. Its main influence on tax policy in the UK was the introduction of tax relief for long-term saving (for example through Tax Exempt Savings Accounts or TESSAs).

There was little interest among countries with the greatest reliance on consumption taxes to increase it further. Instead, the push for taxing consumption more and income less came from a country where consumption taxes were low: the US. This idea was called was called ‘fundamental tax reform’ – and there was an air of fundamentalism about it:

‘I strongly believe that Congress should abolish the income tax system in its entirely and begin anew. A single rate consumption tax on goods and services is the fundamental change needed to spur economic growth and increase wages, saving and investment. Our intrusive tax system should be transformed to one that is fair, transparent and friendly to savings and investment. A sales tax would achieve these goals and allow us to abolish the IRS. Every dollar the American people earn would be theirs to save, spend or invest. They would not have to account for it or face intrusive audits. They could pass it along to loved ones without strings attached.’

Senator Lugar, January 20, 1999 press release.

Proposals to replace US income taxes with a federal consumption tax have not centred on sales taxes like the Australian GST, perhaps because the US States already have sales taxes of their own. In 1977 the US Treasury, in its ‘Blueprints for Basic Tax Reform‘, proposed a progressive expenditure tax similar to Meade’s proposal. This would have been levied at progressive rates, and would have replaced the federal income tax. It would have exempted income from investment and taxed withdrawals from savings accounts. Business would be taxed on cash flow rather than income. ‘Blueprints’ also raised an alternative option – a more comprehensive income tax – and this proposal (not the progressive expenditure tax) was the launch pad for the Reagan tax reform a decade later (discussed in Part 1 of this series).

‘Blueprints’ was followed in 1983 by the ‘flat tax’ proposed by Hall and Rabushka, a tax on business cash flows coupled with a flat tax on wages above an annual threshold. Not surprisingly, this was widely opposed on equity grounds with studies finding it would increase inequality in both the short and long term.

In 1985 Bradford proposed his ‘X Tax’. This was similar to the ‘flat tax’ except that wages would be taxed at progressive rates and business cash flow would be taxed at the top personal tax rate. The ‘X Tax’ was clearly more progressive than the ‘flat tax’ but as with other expenditure taxes, replacing the income tax with the ‘X Tax’ would have benefited those with the ability to save a large share of their income (who are generally relatively well-off), and devalued the savings of retirees.

The push to replace US federal income taxes with an expenditure tax has been spectacularly unsuccessful. In the absence of a federal sales tax, the US relies less on general sales taxes than virtually any other OECD country. As in the UK, the expenditure tax debate led to new tax breaks for long-term saving, but their impact on household saving levels is disputed.

Fundamental tax reformers in the US over-reached in trying to achieve the toughest goal in tax reform – introducing a completely new tax:

‘Replacing the entire income tax with a consumption tax would be a grand experiment of applying theory to a practical application that no other country in the world has chosen to undertake. Proponents of these plans must, therefore, overcome a significant hurdle – they must show that it is worthwhile to conduct this experiment on the world’s largest and most complex economy.’ (former) Assistant Secretary for Tax Policy, Les Samuels, June 7, 1995 testimony.

What happened in Australia?

The strongest push to raise taxes on consumption here came in 1984 with Treasurer Keating’s ‘Option C’. This would have replaced existing consumption taxes with a broad based consumption tax (GST) at 12.5%, enough to pay for substantial income tax cuts. While not opposed to a GST in principle, both ACOSS (representing the community sector) and the ACTU (representing unions) opposed a large consumption tax due to its impact on the cost of living, and equity. At the national tax summit, business representatives opposed all three options because they were not prepared to support the removal of income tax shelters in ‘Option A’ (which included a Capital Gains Tax and a Fringe Benefits Tax).

Once Prime Minister Hawke realised that none of the key sectors were prepared to support ‘Option C’, he pulled the plug. The income tax reforms in ‘Option A’ were introduced regardless, and used to pay for more modest income tax cuts. The business sector learnt its lesson: following the Tax Summit the CEOs of large businesses established the Business Council of Australia to help it formulate common policy positions to take to Government.

This left the consumption tax base in disarray. The Wholesale Sales Tax only taxed goods and not services, yet services were growing in economic importance. State excise taxes on petrol, alcohol and tobacco were later struck down by the High Court on constitutional grounds, and many of the other State indirect taxes, especially Stamp Duties, were widely regarded as economic inefficient. Along with the US, Australia was one of the few OECD countries without a broad based tax on consumption.

The next attempt to introduce one was a crazy-brave push from Opposition in 1993 by the Coalition Parties led by John Hewson. His ‘Fightback’ package would have progressively replaced industrial awards with individual contracts, abolished Medicare, placed time limits on unemployment benefits, and introduce a Goods and Services Tax. Coming after a recession when people craved economic security, ‘Fightback’ scared voters and the Labor Party won the election.

Hewson’s proposed GST rate was 15% and this would have funded a 30% reduction in income taxes as well as replacing existing consumption taxes (since the GST would have replaced State Payroll Taxes as well as the Wholesale Sales Tax, the proposed change in the tax mix towards consumption was not as large as ‘Option C’).