Business, Government, and “every pet shop galah” have been saying that we should rely less on personal income taxes and more on the GST because this would be good for the economy. In my blog ‘Who’s the fairest and most efficient of them all?” earlier this year, I challenged this view.

Treasury modelling of the economic impact of different taxes tucked away on p32 of the Government’s Tax Discussion Paper confirms my doubts. It should change the debate.

Now, Treasury has released the details of that modelling.

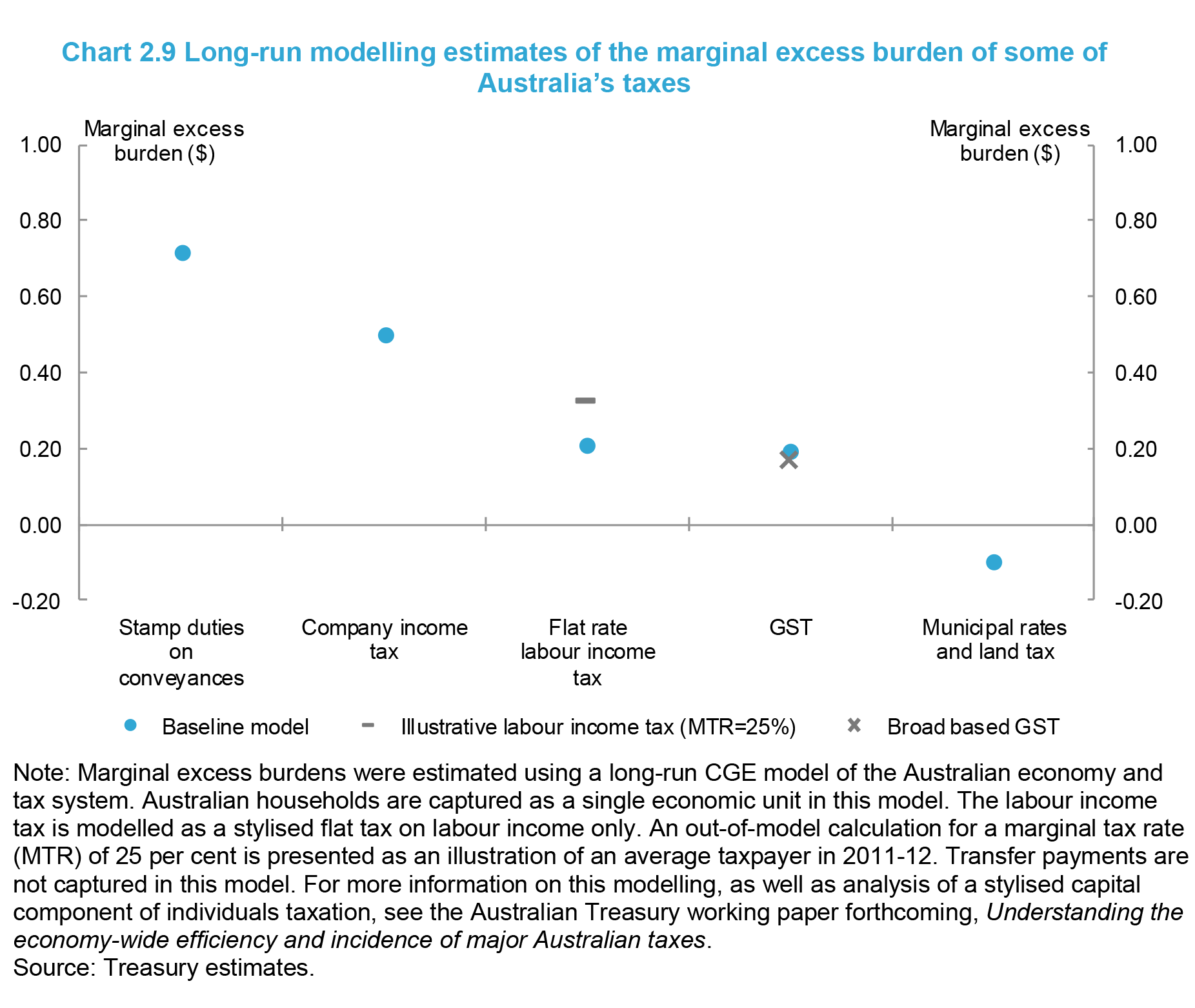

Here’s the graph from the Discussion Paper comparing the “marginal excess burden” (efficiency loss) of different taxes. The marginal excess burden is the loss of future spending power across the economy per dollar of revenue raised from a tax. A low MEB means a tax is efficient; a high one suggests we might look elsewhere for public revenue.  The “efficiency ranking” of taxes here is similar to other studies, with taxes on land the clear winner and Stamp Duties receiving the wooden spoon. Company income tax is growth-reducing to the extent that capital is mobile (and the assumptions the model makes about this are critical).

The “efficiency ranking” of taxes here is similar to other studies, with taxes on land the clear winner and Stamp Duties receiving the wooden spoon. Company income tax is growth-reducing to the extent that capital is mobile (and the assumptions the model makes about this are critical).

Comparing labour income taxes and GST: economically, there’s nothing in it!

But the real story is the comparison between income taxes on labour and the GST: if the Treasury’s modelling is accurate there’s nothing in it! The MEB for a flat rate income tax on labour incomes was 21%, that for the GST 19%. Contrast this with Stamp Duties at 72%, and there’s nothing in it. A flat-rate labour income tax is about as efficient as the GST (compare the two blue dots in the graph).

“Our estimate of the marginal excess burden on individual’s labour income and GST are very similar at around 21 cents and 19 cents respectively. This aligns with the intuition that taxation of labour income and GST both effect the real purchasing power of wages, with a similar incidence on labour supply.”

and:

“Compared to taxes with a relatively significant impact on economic growth and living standards (such as company tax), individuals income tax is usually considered to have a comparatively moderate impact on the behaviour of most people, and relatively minor adverse impacts on economic growth and living standards”, p41

It turns out that consumption taxes also reduce work incentives, because they reduce the spending power of wages. Indeed, tax theory suggests that consumption taxes fall more heavily on labour (and the accumulated savings of retired people) than income taxes. So a shift from taxing income to consumption is likely to reduce work incentives overall – This is argued in my blog ‘Who’s the fairest and most efficient of them all?’

Treasury’s modelling suggests that a progressive income tax (in which tax rates rise with income, represented by a dash in the graph) is less efficient than a flat one (in which tax is levied at the same rate on everyone, represented by a dot).

But here there’s a glitch in the model. Households are represented by a single family, so the model is unable to distinguish between work incentives for men and women, two income families and single income families, or families with and without children. The model simply assumes that as income tax rates rise, they have a greater (negative) impact on workforce participation. And it does not take into account the combined impact of income tax rates and social security income tests, which mainly impact on unemployed people and women in low and middle income families.

As the Treasury knows, in the real world it is low-income women not high-income men who are most sensitive to taxes when they decide whether to increase their paid working hours:

“The groups most likely to respond to high effective tax rates include the unemployed and

lower-income earners (who often work part-time). Primary care givers, such as parents with young children, are also relatively responsive to effective tax rates but they also respond to other costs associated with working, such as child care.” p45and:

“In the absence of any changes to payments or assistance, and all else being equal, targeting tax cuts at the lower end of the income spectrum should generate a higher participation response than if the same value of tax cuts were delivered at higher incomes, “p45.

So it’s not obvious that a progressive income tax is worse for labour incentives than a flat income tax. There’s a body of research that suggests the opposite.The highest income tax rates fall on married men, and the sensitivity of the working hours of married men to an increase in tax is close to zero in research cited by Treasury.

Broadening the GST: nothing in this either

The other eye opener is the difference in the economic impact of the current GST (which taxes about half of all consumption, represented by a dot in the graph) and a broad based one (which taxes all consumption, represented by an x). Again, there’s nothing in it, a difference of just 2%!

It might be tough for retailers to distinguish between the GST treatment of a pizza and a pizza roll, but it makes little difference to growth levels in the wider economy.

Income taxes and investment: more of a story here

The Treasury modelling also challenges the view that a switch away from taxing personal income would be good for investment, arguing that investment is more sensitive to global rates of return than the impact of local taxes on investment incomes.

On the other hand, it concludes that foreign investors are very sensitive to company income tax rates. The MEB for company tax is estimated at 50%. Treasury argues that company taxes ultimately fall largely on workers as a result of lower foreign investment in Australia. There are two critical assumptions here: perfect capital mobility (without which Treasury says the MEB could fall by 20%) and that ‘economic rents’ comprise about one seventh of profits taxed in Australia (if this is doubled then the MEB also falls by about 20%).

Economic rents are above-normal profits flowing from location or firm specific inputs such as natural resources. If they are taxed properly, there are virtually no adverse economic impacts because the tax has no effect on investment decisions. So the higher the proportion of company income taxes that come from economic rents, the less likely they are to have adverse impacts on the economy.

The tax that dare not speak its name – a properly designed mineral resources tax – is a tax on economic rents. This was the main reason the Henry Report argued for a switch from taxing company income generally towards a tax on above-normal profits from mineral resources.

The ideal tax: Land

Finally, since land is immovable, a broad based tax on all private land (such as council rates) has no adverse economic impacts. Indeed, the Treasury estimates it would improve economic efficiency by 10%. This positive view of the economic effects of a broad tax on Land is uncontroversial.

Don’t always believe what you read in the papers

This is a timely warning for Government, tax lobbyists, the media, and tax reform junkies. Don’t always believe what you see and hear in the news.

It’s also a warning about tax reform modelling. It’s a very imprecise science. Many people have quoted the findings of a 2008 OECD study which found that consumption taxes were more efficient than taxes on personal income. A close reading of that report reveals the caveats:

‘Estimates of the effect on GDP per capita of changing the tax mix while keeping the overall tax-to-GDP ratio constant indicate that a shift of 1% of tax revenues from income taxes to consumption and property taxes would increase GDP per capita by between a quarter of a percentage point and one percentage point in the long run depending on the empirical specification.The magnitude of the estimated effect is larger than what would be reasonably expected. Given that there is a wide dispersion of the point estimates across specifications it is clear that the size of the effects cannot be measured precisely in a cross-country comparative setting. …Thus, the magnitude of the effects should be interpreted with caution.’ (p43)

In contrast to the latest Treasury research, modelling by KPMG Econtech of the impact of different taxes on the Australian economy which was conducted for the Henry Review found that consumption taxes were significantly more efficient than personal income taxes (though the overall efficiency rankings of different taxes were the same as above).

This raises a serious question for policy makers: is our economic modelling of the impact of taxes reliable enough to draw firm conclusions for policy? This question was posed recently by a study commissioned by the Mirrlees review in the UK. The authors concluded that arguments for the removal of taxes on investment incomes were getting well ahead of the reliability of the research.

If the impact of greater reliance on consumption taxes on the economy is uncertain, its (regressive) impact on household spending power is clear. (see my blogs: ‘Who’s the fairest and most efficient of them all?’ and ‘ACOSS report shows taxes are lower and less progressive than people think.’)

It’s time to move on from the unproductive and divisive debate over whether to tax consumption more and income less, and get down to the business of making both income and consumption taxes fairer and more efficient. There’s plenty that needs to be done.

Thanks a lot for your blog posts, Peter, they are great! For your information, none of the hyperlinks you have to your own posts work for me (they seem to link to the editing tool for the respective posts, rather than the posts themselves).

LikeLike